Stock Markets

Stocks advanced to near record highs this week thanks to improving economic data, supportive global central-bank policies, and new optimism around the trade issue that has been plaguing the markets. In a positive move, China announced that it would exclude certain U.S. products from tariffs. The U.S. immediately provided a “good dog” response by delaying the increase for some of its tariffs that are scheduled to take effect in October. These small mercies by both sides appeared to lift optimism that it is possible to reach an interim trade agreement. Market moves last week included a major rise in Treasury yields along with the outperformance of typical cyclical sectors such as industrials, financials, and energy versus defensives stocks such as health care, staples and utilities. There was also a shift in the preference for stocks with depressed valuations over stocks that traditionally trade at higher price-to-earnings ratios.

U.S. Economy

The stock market’s rebound from the August pullback is no surprise. It remains consistent with analysts’ view that equities will likely see more volatility at this stage in the cycle, set against a fundamental backdrop that still supports the extension of this bull market. Things cooled slightly on the geopolitical front in September so far, but the core contributors fueling the bouts of volatility have not been eradicated. It’s likely that the Fed will cut rates this week, but viewers expect markets will respond to any signals that additional policy moves aren’t in sync with current expectations for more rate cuts. Also, despite signs of progress, most don’t expect the trade situation with China to reach an end soon, keeping markets volatile. The important Brexit issue is likely to get a lot of attention on the horizon.

Metals and Mining

Gold regained further momentum Friday as the US dollar slumped, based on concerns surrounding a global growth slowdown. Although it was up, gold was capped by equity markets that were gaining thanks to a potential respite in the US-China trade tensions. Analysts feel that that continued fears surrounding a global economic downturn and negative-yielding government debt, married to a dovish monetary policy outlook by global central banks will support gold long-term. Experts in the gold market continue to predict increasingly high levels for the metal’s price. Silver was also up slightly on the back of a lower dollar and ongoing global economic tensions. Since it tends to follow the path of gold, many investors believe that it too is still in a great position to continue strong gains as it has been since early August. In other other precious metals, platinum was up on Friday, continuing to trade above the US$900 per ounce level. Platinum prices have surged over the last month thanks to greater safe haven demand paired with supply concerns.

Analysts see the price of the metal rising slightly, but they feel it will trail behind its sister metal palladium. On that side, palladium lost on Friday after experiencing an all-time high during the previous session that peaked at US$1,621.55. Analysts feel palladium prices may dip, but it will continue to be supported throughout the year. Next week, market participants will be keeping a close eye on $1,500 gold pricing as the first line of defense gold prices have to hold in the near term, according to analysts.

Energy and Oil

The series of back-and-forth gestures between Washington and Beijing has boosted market sentiment. Chinese firms bought 10 shipments of U.S. soybeans on Thursday in another effort to build confidence inspiring the October trade talks. Politico reports that the Trump team is trying to find an ease the trade war that the President started. There is a growing effort to head off trade escalation. However, a breakthrough in negotiations is a serious challenge. Oil remains tight now with a surplus in 2020. The IEA said this week that the market will see inventory drawdowns of 0.8 mb/d in the second half of 2019, but that a surplus would return in 2020. The request to OPEC is set to decline by 1.4 mb/d next year. This will present a serious situation for the cartel to resolve. Natural gas spot prices rose at most locations this week. Henry Hub spot prices rose from $2.42 per million British thermal units (MMBtu) last week to $2.59/MMBtu this week. At the New York Mercantile Exchange (Nymex), the price of the October 2019 contract increased 11¢, from $2.445/MMBtu last week to $2.552/MMBtu this week. The price of the 12-month strip averaging October 2019 through September 2020 futures contracts climbed 9¢/MMBtu to end at $2.561/MMBtu.

World Markets

European stock markets were up this week as the European Central Bank announced new monetary stimulus aimed at supporting the eurozone economy. At the same time, fears of a no-deal Brexit were waning. The pan-European STOXX Europe 600 Index rose about 1.3%, the German DAX gained 2.4%, and the UK’s FTSE 100 Index rose 1.2%. The British pound rose to its highest level against the U.S. dollar since July. That’s due to Parliament passing a law that forces the UK government to seek a Brexit extension from the European Union as well as avoids a no-deal Brexit on October 31. The German Ifo Institute cut its forecast for German growth this year to 0.5% from 0.6% and lowered its estimate for next year to 1.2% from 1.7%.

Chinese stocks advanced in what was a holiday-shortened week. Both China and the U.S. took important steps toward reducing their trade war. Expectations also increased that Beijing would be putting more stimulus measures in place to boost the economy. For the week ended Thursday, the benchmark Shanghai Composite Index rose 1.1%, its highest level in 10 weeks. The large-cap CSI 300 Index added 0.6%. Stock markets on the mainland were closed Friday for the Mid-Autumn Festival.

The Week Ahead

This week’s focus will be primarily on the Federal Reserve as it issues its latest rate decision this Wednesday. There are other important economic figures emerging during the week as well including housing starts, industrial production numbers, existing home sales, along with Friday’s figures on the leading economic index.

Key Topics to Watch

- Empire state index

- Industrial production

- Capacity utilization

- Home builders’ index

- Housing starts

- Fed announcement

- Jerome Powell press conference

- Weekly jobless claims

- Philly Fed survey

- Current account deficit Q2

- Existing home sales

- Leading economic indicators

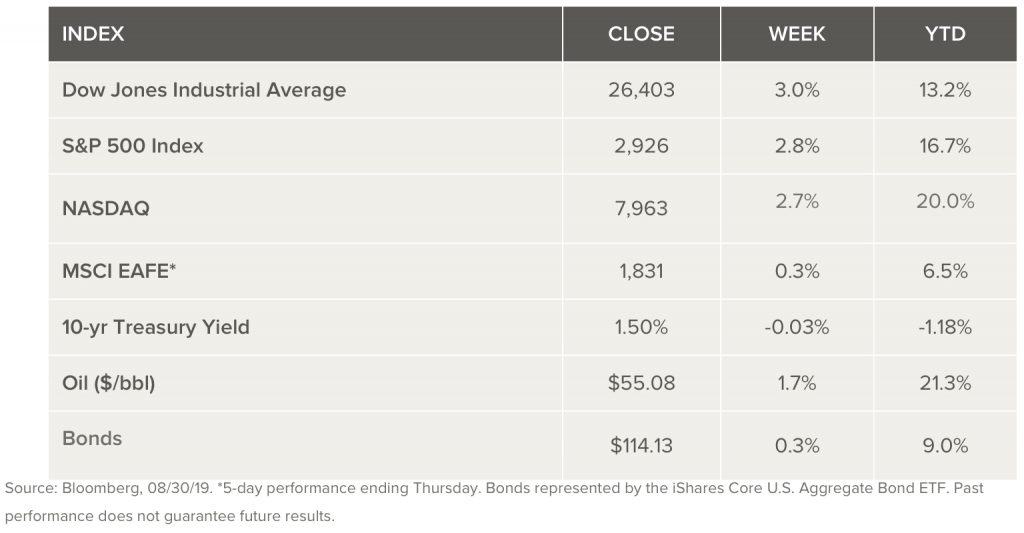

Markets Index Wrap Up