Investing in retirement requires a different focus, usually one that includes a prominent place for dividend income. If dividend-paying stocks are what you’re looking for, then you should take a closer look at high-yielding Duke Energy Corporation (NYSE: DUK), ONEOK, Inc. (NYSE: OKE), and W.P. Carey Inc. (NYSE: WPC). They offer dividend yields of 4%, 5%, and 6%, respectively… income that could materially increase your retirement “paycheck” and help to supplement Social Security.

1. The giant utility

Duke Energy is one of the largest utilities in the United States. It offers a dividend yield of around 4.4% today, and has increased its dividend annually for 13 consecutive years. It’s actually a pretty boring stock, but that’s part of its charm: It has a tiny beta of 0.1, suggesting the stock is roughly 90% less volatile than the broader market. Duke is something of a cornerstone investment in that regard, adding stability to a diversified portfolio.

The high-yield utility has plans to spend nearly $50 billion on capital expenditures between 2018 and 2022 across its electric and gas businesses. That will support its requests for regulated rate increases, and should lead to 4% to 6% earning growth each year, on average, over that span. The dividend, meanwhile, is expected to grow along with earnings, easily keeping up with the roughly 3% historical growth rate of inflation. Duke probably won’t excite you, but that’s why you’ll want to own it.

2. Growing pipeline profits

Midstream pipeline operator ONEOK is a bit more exciting, offering investors a 5.2% dividend yield backed by 16 years of annual dividend increases. It’s worth noting that it is not structured as a limited partnership, which is common in the midstream space. That means it can be owned in a tax-advantaged retirement account without causing any tax headaches.

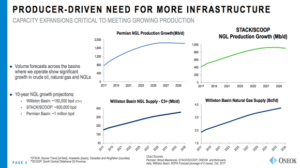

ONEOK has three main goals today: Invest for growth, reduce leverage, and increase the dividend by a huge 10% a year. On the growth front, the midstream company sees demand for its assets increasing along with oil and gas production from key U.S. energy regions like the Permian and Williston basins. It currently has around $4.2 billion in growth projects that will be completed between 2018 and 2020 to serve that growing production.

As those assets come on line, the company’s largely fee-based revenues will head higher, and that should help it to reduce its leverage. It has already been able to push debt to EBITDA from 6.7 times in 2013 to 4.6 times at the end of 2017. The goal is to get to 4 times on that metric. While it’s trimming leverage, it also plans to keep rewarding investors with the goal of 9% to 11% dividend growth through 2021, with a robust coverage ratio of 1.2 times. So far it’s executing well on its trio of goals. If you are looking for a mixture of high yield and dividend growth, ONEOK is worth a deep dive today.

3. A diversified, high-yield property owner

Last up is W.P. Carey, which is a “triple net lease” real estate investment trust, or REIT. With a triple net lease, the landlord owns the building, but the tenant is responsible for most of the costs, including taxes and maintenance. Carey specializes in sale/leaseback deals, in which a company sells a key property to generate cash or reduce debt and then instantly rents it back under a long-term lease. This model has worked well for the REIT and its shareholders, who have been rewarded with 21 consecutive annual dividend increases. The current yield, meanwhile, is a robust 6.6%.

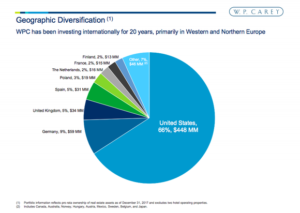

Carey distinguishes itself from peers through its diversified portfolio. While many triple net lease REITs are focused on retail assets, Carey’s portfolio is spread across industrial (30% of its base rents), office (25%), retail (17%), warehouse (14%), self storage (5%), and other (the remainder). It also gets about a third of its rent roll from Europe, providing geographic diversification as well.

It’s worth noting that Carey tends to actively manage its portfolio. That means it buys and sells assets on a regular basis, often looking for opportunistic situations that are out of sync with the broader market. For example, it had specifically avoided U.S. retail for years because management believed the country had too much retail property — a decision that has since proved prescient. It focused, instead, on retail assets in Europe, a region with much less retail space.

If you are looking for a diversified and well managed property owner offering a high yield, Carey should be on your short list. That said, the yield is likely to provide most of your returns, and you should only expect dividend growth to track along with inflation, or slightly higher, over time. But if you are looking to generate a high level of current income, then this shouldn’t be a big deal.

A trio of income plays

Duke, ONEOK, and Carey are three high-yield dividend payers that span a broad spectrum of income opportunities: a boring, steady utility; a growth-oriented midstream energy company; and a high-yield REIT that actively manages its diversified triple net lease portfolio. They may not all be right for your retirement portfolio, but if you take the time to get to know these stocks, I’m confident that at least one could find a place in your income portfolio today.