Long-term business tailwinds and market-trouncing dividends have made Verizon Communications (NYSE: VZ) a staple in income investors’ portfolios. But Verizon isn’t the only top stock that’s rewarding investors with an envy-inspiring yield. BP PLC (NYSE: BP), Ford Motor Company (NYSE: F), and AT&T Inc. (NYSE: T) offer higher yields than Verizon does, and according to three Motley Fool contributors, each has catalysts that could make now the perfect time to add it to your income portfolio.

Time to warm up to energy

Todd Campbell (BP PLC): Energy exploration and production stocks took a drubbing after crude oil prices peaked in 2014, but commodity prices have been marching higher for over a year now, and that’s translating into increased profits at companies like BP.

One of the biggest energy producers on the planet, BP has its hands in upstream (finding and extracting oil and gas), midstream (transport, including pipelines), and downstream (selling to consumers) businesses.

Last quarter, BP reported its best quarterly profit in three years. I expect that we’ll see more of those “bests” as some very important new projects come online.

In 2017, the company started up seven new projects — on time and under budget — and as a result, its upstream production grew 14% year over year last quarter. In 2018, six new projects are coming online, including Atoll in Egypt and the massive Shah Deniz in the Caspian. Between 2016 and 2021, BP’s goal is to add 1 million new barrels of oil production per day.

Higher prices for that higher production could be a big driver of future profit growth, but BP’s also benefiting from operating leverage because of its cost-cutting during the downturn. According to management, margins on major projects through 2021 will be, on average, over a third higher than margins were on production in 2015.

BP’s also growing downstream by entering new markets, like Mexico, where it has 200 locations currently, and it’s expected to have 1,500 locations by 2021. BP’s also getting in on the renewable energy boom via its Lightsource partnership, and it hopes to grow its midstream business via a spin-off it did last year, BP Midstream Partners.

Overall, it’s hard to predict where oil and gas prices are heading, but it appears that the worst is behind BP. If so, then buying it now may pay off in more than the chance to collect its 5.35% dividend yield.

Hello, China

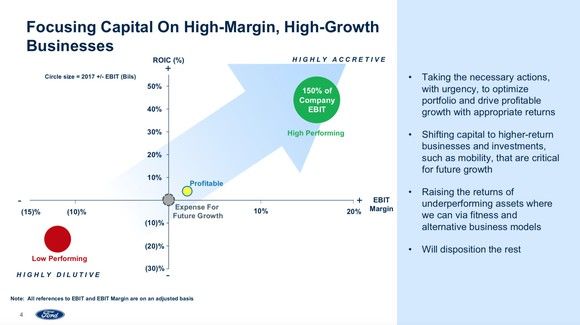

Daniel Miller (Ford Motor Company): If you’re scanning the market for dividends paying more than Verizon’s, take a look at Detroit’s second-largest automaker and its 5.3% yield — and that figure doesn’t include its annual supplemental dividend. Yes, new vehicle sales in North America have peaked, but Ford is determined to slash its budget, focus on SUVs, and expand in China. All those factors should help power Ford’s bottom line in the near term.

Last month, Ford announced its largest new vehicle launch in China. Those launches include the new Focus, Escort, and Ranger Wildtrak, as well as the Lincoln Aviator, MKC, and Nautilus. It’s the first wave of the 50 new products Ford plans to launch in China by 2025, in an attempt to capitalize on the world’s largest automotive market.

Meanwhile, back in the heartland, Ford is doubling down on cost-cutting. Originally Ford’s cost-cutting goal was $14 billion, a figure that was plenty big. Now, CEO Jim Hackett has bumped the cost-cutting target to a staggering $25.5 billion and expects to reach 8% global profit margin by 2020 (Ford’s global profit margin was 5.2% during the first quarter). It’s even possible that Ford could exit certain geographic regions and markets if reasonable returns aren’t viable in the medium term, similar to General Motors’ move to sell its European operations.

Ford is an intriguing automaker as it expands in China, cuts costs to boost the bottom line, and dishes out a juicy 5.3% yield. But to be more than a dividend stock for income investors, the company must find a way to generate revenue from the coming driverless-car trend.

A fallen Dividend Aristocrat

Leo Sun (AT&T;): Verizon’s rival AT&T; pays a forward dividend yield of 6% — its highest yield since 2011. That yield was inflated by the stock’s 17% year-to-date decline, which was caused by concerns about the sluggish growth of its postpaid smartphone, wireline, and pay-TV businesses. AT&T’s planned takeover of Time Warner, which could transform it into one of the biggest media companies in the world, also remains in limbo.

Yet AT&T is still the second-largest wireless carrier in the US, and the nation’s top wireline and pay-TV service provider. Those businesses give it a wide moat against its potential challengers, and the telco has rebounded from plenty of market downturns in the past.

AT&T generated $18.3 billion in free cash flow over the past 12 months, and spent just 66% of that total on dividend payments. That gives it plenty of room to hike its payout, as it did annually for 33 straight years. That streak makes AT&T an elite “Dividend Aristocrat” — a member of the S&P 500 which has raised its dividend for over 25 straight years.

Wall Street expects AT&T’s revenue to slip 3% this year, but its earnings — boosted by buybacks, potential divestments, and better cost controls — to rise 12%. AT&T’s big drop reduced its forward price-to-earnings ratio to just 9, which is lower than Verizon’s multiple of 10. Therefore, I think AT&T’s downside is fairly limited at these prices.

Image source: Ford Motor Company.

Image source: Ford Motor Company.