Utility stocks can provide a solid cornerstone to an investor’s income-focused portfolio. In fact, if you pick the right ones, they will reliably provide you big dividends and very little excitement, which is likely your goal. American Electric Power Company, Inc. (NYSE: AEP), Consolidated Edison, Inc. (NYSE: ED), and CenterPoint Energy, Inc. (NYSE: CNP) are three such stocks that offer a combination of high yields in the utility space backed by financially strong businesses. Here’s why dividend investors will love them.

1. American Electric Power

AEP provides electricity to 5.4 million customers across 11 states. The utility has three main business, regulated utilities, regulated transmission and distribution utilities, and AEP Transmission. It has increased its dividend each year for eight consecutive years and offers investors a 3.7% dividend yield. That’s well above the roughly 2% yield the broader market is offering investors today and toward the high end of the utility group.

Leverage at AEP is relatively modest for a capital intensive industry, with a debt to equity ratio of just 1.06 times. That’s a level that’s been fairly consistent over the past decade. The company is investment grade rated, as well, at A-. The payout ratio, meanwhile, was a strong 62% in 2017.

AEP is projecting earnings growth of between 5% and 7% a year. The dividend should track along with those gains, extending the company’s streak of annual hikes along the way. Capital spending of nearly $18 billion backs those projections over the next two years. Better yet, the dividend growth of 5% plus will outpace the historical rate of inflation growth.

2.Consolidated Edison

ConEd serves 3.6 million electric and 1.2 million natural gas customers in New York City and its surrounding suburbs. It breaks its business into utilities, transmission (which owns assets that move both natural gas and electricity), and renewable power (which sells renewable energy under long-term contracts). The utility has increased its dividend for an incredible 44 consecutive years. Like AEP, ConEd’s current yield is roughly 3.7%.

Consolidated Edison’s debt to equity ratio is the lowest of this trio at just 0.96. It’s been below one on that metric in nine of the last 10 years, proving that management is focused on maintaining a solid balance sheet. The utility’s credit rating is investment grade at A-. The payout ratio, meanwhile, was around 70% in 2017. It’s held at around that level for the past decade.

ConEd’s capital spending plans are heavily weighted toward its most important business.

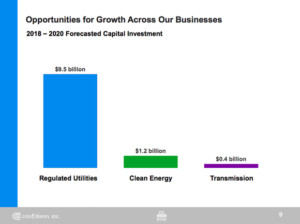

The company plans to spend around $11 billion on capital projects between 2018 and 2020, with the vast majority going toward its regulated utilities business. Although ConEd hasn’t provided longer-term earnings and dividend growth projections, it believes 2018 adjusted earnings could rise by as much as 5% and it has already increased the dividend by 3.5%. That’s not a huge dividend hike, but it’s above inflation and backed by a rock solid utility.

3. CenterPoint Energy

CenterPoint provides electricity to 2.4 million customers in Texas and natural gas to 3.5 million customers across six states. It also owns roughly 54% of the common units of Enable Midstream Partners, LP which it jointly controls with OGE Energy Corp, a midstream infrastructure specialist. CenterPoint’s yield is 4.15%, more than twice the broader market’s yield. The utility has increased its dividend annually for 13 consecutive years.

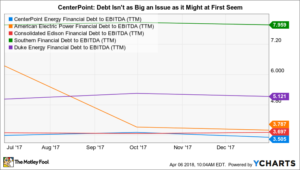

Although CenterPoint’s debt to equity ratio is higher than AEP’s and Con Ed’s at 1.75 times, its debt to EBITDA ratio is slightly lower. That suggests it isn’t particularly over leveraged relative to these peers, particularly when you compare it to industry giants like The Southern Company and Duke Energy, which have much higher debt to EBITDA ratios. CenterPoint also has a solid A- investment grade credit rating. The payout ratio in 2017, meanwhile, was roughly 75%, which provided ample coverage for the dividend.

CenterPoint is targeting 5% to 7% earnings growth through 2020. Backing that is an $8 billion capital spending plan between now and 2022, split roughly 60%/40% between its electric and natural gas businesses. In recent years the dividend has grown at around 4% as the utility has worked to reduce its payout ratio. It’s likely that dividend growth will remain at that level for now, a move that would continue to increase the security of the payout.

Core dividend holdings

AEP, ConEd, and CenterPoint each have solid utility business with investment-grade credit ratings. Relatively low leverage and ample dividend coverage should leave most income investors confident that the dividends will keep flowing from this trio. Add in above market yields and it’s likely that at least one of these utility stocks could find its way into your portfolio.