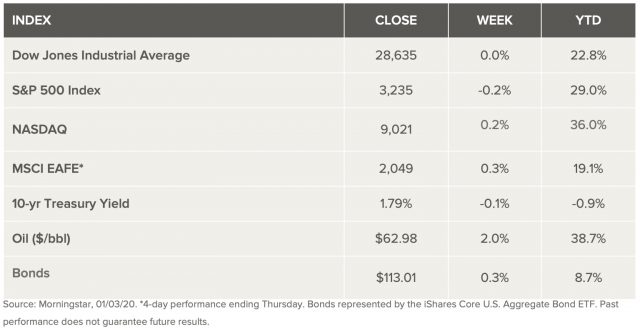

Stock Markets

What analysts call better-than-expected economic data, encouraging corporate earnings from U.S. banks, and the signing of the “phase-one” trade agreement helped raise U.S. stocks to fresh record highs last week. A surge in housing starts bolstered by strong retail sales point to a resilient consumer that is supported by a continued strong labor market. The “phase-one” trade agreement between the U.S. and China was formally signed last week, fulfilling expectations for a deal that was already done. Important terms of the deal included commitments from China to increase purchases by $200 billion over the next two years ($78 billion of manufactured goods, $52 billion in energy, $32 billion of agricultural products, and $38 billion in services). Analysts agree that the agreement removes significant uncertainty, however, they say trade issues will likely continue as a source of volatility through 2020.

U.S. Economy

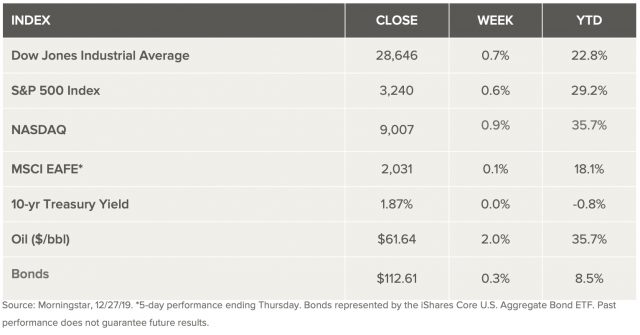

The closing of stocks at record highs last week was driven by the U.S. and China reaching the “phase-one” trade agreement. Analysts believe the recent trade agreement is a significant step in the de-escalation of the trade tensions between the two superpowers. It takes away much of the threat that new tariffs create and creates confidence that a more comprehensive deal is achievable. Still, tariffs remain in place on two-thirds of U.S. imports from China. So, attention now shifts to implementation and enforcement. Potential failure to meet the terms of the deal could create temporary setbacks which could stretch as far as additional new tariffs. Further tariff relief and more complete trade cohesiveness that would include including structural fundamentals, like industrial subsidies, is likely to be in place by the time we reach the U.S. election. The current agreement gets rid of significant uncertainty, but all agree that trade issues will likely create some volatility in the coming year. Analysts expect stocks to continue to rise but at a slower pace than they have over the past decade. This is widely supported by ongoing economic growth, modest earnings growth, and accommodative central banks.

Metals and Mining

The precious metals sector was two sided this week, with gold and silver remaining in a channel, while both platinum and palladium climbed. Platinum was up 4.4 percent from last week, exceeding US$1,000 per ounce for the first time in two years. The precious metal had been sidelined for much of the growth that palladium and gold experienced in 2019. Now it’s starting to see a benefit from the same motivators that drove those metals. Rallying from US$976 (January 10) to US$1,037 (January 16), Platinum exhibited its best performance year-to-date. It is on track to surge to highs not experienced since 2015. The phase one trade deal between China and the US countered some of the volatility that entered the market earlier in this month. The exchange traded-funds sector (ETF) may help motivate the platinum’s price too, since last year, platinum ETFs grew by 12 percent with investors purchasing 90,000 ounces or 11 percent of global supply. Easing geopolitical tensions moved against gold’s momentum, putting it on course to record its weakest performance in nearly two months. News of the phase one deal pushed gold below US$1,550 only to rebound supported from a weaker equity market and lower US dollar. Another round of increased buying from central banks and monetary policy are also projected to impact the value of gold in 2020. Palladium continued its upward trend this week. The precious metal star climbed 14 percent to trade at an all-time high of US$2,429 on January 17. Palladium’s hyperbolic performance has now moved the industrial metal beyond platinum and gold’s record highs, making it the most valuable of the four exchange-traded precious metals. The German bank pointed to the prolonged supply deficit as the current catalyst behind palladium’s best historic performance. Like gold, silver remained locked in a range staying below US$18 an ounce for much of the week. Silver has exhibited the poorest price growth of all four precious metals. It ended the week without any gains.

Energy and Oil

As expected, China has been the key oil price driver this week. The phase one trade deal drove prices higher before worrying economic data from the country dragged prices lower. Oil prices regained a bit of ground by week’s end. That was based on optimism surrounding the Phase 1 U.S.-China trade deal only. The global oil market managed to dodge a bullet after the U.S. and Iran backed away from war talk and eased tensions. But the geopolitical risk has not disappeared. In any case, non-OPEC oil supply is expected to continue to grow faster than demand this year. Once again that leaves the market with a persistent supply surplus, according to the IEA. The result is tremendous pressure on OPEC+, which may find that it needs to cut even further than current levels. In the U.S. Permian basin, the industry is suffering through bankruptcies, slower growth and investor scrutiny. Many analysts suggest that production should grow this year, however skeptical investors are starting to see a potential for peak in supply over the near-term period. Natural gas spot price movements were mixed this week. The Henry Hub spot price fell from $2.08 per million British thermal units (MMBtu) last week to $1.98/MMBtu this week. At the New York Mercantile Exchange (Nymex), the price of the February 2020 contract decreased 2¢, from $2.141/MMBtu last week to $2.120/MMBtu this week. The price of the 12-month strip averaging February 2020 through January 2021 futures contracts declined 3¢/MMBtu to $2.290/MMBtu.

World Markets

Stock in Europe rose this week as trade tensions eased, and investors welcomed strong Chinese economic data. The pan-European STOXX Europe 600 Index ended the week 1.33% higher, and the UK’s FTSE 100 Index gained 1.30%. Germany’s DAX Index advanced 0.3%. For the UK, poor economic data, combined with recent dovish speeches and comments by Bank of England (BoE) Monetary Policy Committee (MPC) members, set speculation in motion that an interest rate cut is in the cards at the January 30 policy meeting. What was suggested as a quarter-point reduction in the benchmark Bank Rate, from 0.75% to 0.50%, just rose to 80% on expectations. Analysts see rate cut as a form of insurance given the sharp slowdown at the end of the year. This move that probably should have occurred at the end of 2019 but was weigh laid by the general election. Analysts also expect data to begin improving as uncertainty has receded since the Conservative Party election victory, so purchasing managers’ surveys of the construction, manufacturing, and services sectors, will still be key to policymakers’ voting intentions.

China’s stock market moved slowly ahead of the signing of the phase one trade deal with the U.S. and did not rebound after the announcement. The Shanghai Composite lost 0.8% during the week while the CSI 300 large-cap index edged down 1.2%. The trade deal was already baked into the market came largely as expected. Many observers in the region viewed the deal as driven primarily by U.S. election politics and as a band-aid rather than a solution. For its part, China has pledged to import much more from the U.S. There are worries that the target of a USD 200 billion increase in imports of goods and services from the U.S. over the next two years may be very difficult to achieve and could fall short. Regional skeptics also doubt China’s claim that other countries will not suffer as it redirects purchases back to the U.S.

The Week Ahead

U.S. markets will be closed on Monday to observe Martin Luther King Jr. day. Important economic data being released include pending home sales, the leading index on, and the Markit Purchasing Managers’ Index on Friday. This is an important week in the corporate earnings season as another 43 companies of the S&P 500 will be reporting fourth-quarter earnings.

Key Topics to Watch

- Chicago Fed national index

- Existing home sales

- Weekly jobless claims

- Leading economic indicators

- Markit manufacturing PMI (flash)

- Markit services PMI (flash)

Markets Index Wrap Up