Investors don’t buy stocks like Procter & Gamble (NYSE: PG) with the expectation that they’ll witness exciting sales growth or soaring profits. Instead, traits like a diversified product lineup, stability, predictability, and dividend income make the consumer products titan’s shares attractive as an investment.

But P&G can still surprise Wall Street every now and then. Its upcoming earnings report, for example, might have a bit more drama than shareholders are used to seeing. The announcement should clarify for investors whether the company will reach its fiscal-year growth targets, for one. It’s also the first earnings report following a controversial board shakeup, which means the company might articulate a fresh strategic approach to its turnaround targets.

With that in mind, let’s look at some of the key trends to watch for in this report, set for release before the market opens on Friday, April 20.

Growth and market share

P&G is more than halfway through what might mark its third straight year of accelerating revenue growth. Organic sales rose by 1% in fiscal 2016 and then by 2% last year. The company’s latest forecast calls for that figure to come in between 2% and 3% in fiscal 2018, too. That would be enough to beat rival Kimberly Clark (NYSE: KMB), which is looking to expand at a 1% pace in 2018.

However, P&G hasn’t been growing quickly enough to boost overall market share. In fact, it lost ground across each of its main product categories last year, with its Gillette shaving franchise suffering particularly tough losses. That’s a problem since its business model relies on P&G achieving at least modestly market-beating sales growth.

Back in January, the company said it was encouraged to see a moderation in market-share losses. Yet management also noted increased competitive challenges, especially around pricing. Investors will find out on Friday which of those trends won out over the last few months, and whether the latest demand shifts threaten P&G’s multiyear growth rebound.

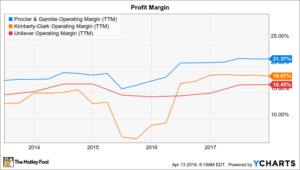

Profits and strategy shifts

Investors should see more clear-cut wins this week on the financial side of the business. Even after slashing over $10 billion from the cost infrastructure, management is still finding plenty of room to cut expenses, and so profitability will likely rise.

P&G is becoming more efficient in its use of capital, too, which is helping free up cash that executives can invest in the business or return directly to shareholders through dividends and stock buybacks. The company just announced its biggest dividend raise since 2013 and hiked its full-year earnings growth target last quarter to as much as 8%. CEO David Taylor and his team will probably stress these financial successes on Friday, especially if sales growth fails to impress.

Finally, it’s possible investors will hear a different tone out of management this week now that activist investor Nelson Peltz has joined the board of directors. After Peltz’s election, which P&G executives fought against, management admitted that they heard a clear message that investors were losing their patience. “There is broad shareholder support for P&G;’s strategies,” they explained in December, but “at the same time, shareholders indicated that P&G; needs to move faster to deliver improved results.”

If this week’s report doesn’t show signs of an accelerated expansion pace, then investors might hear about a new approach that management is working on, one that has a better shot at boosting overall returns for P&G shareholders.