The recent volatility in the stock market can make older investors feel vulnerable. Here are some strategies to make sure your money lasts as long as you do.

You’ve heard it before: When the markets become erratic, or seem poised for a prolonged downturn, the best thing you can do is nothing at all.

But if you’re on the cusp of retirement — or, perhaps worse, newly retired — a turbulent stock market can make you feel particularly vulnerable.

While there’s some validity to those feelings, it’s more productive to redirect any panic into prudence, which will help ensure your money lasts longer.

For older people invested in stocks, the performance of the market in the early years of your retirement can have a lasting effect on your portfolio, which will remain a dynamic entity for perhaps three more decades. If you have to start selling investments when they are worth less, you’ll have to to sell more shares to get the cash you need — and the repercussions build on themselves.

“That can really start digging a hole in your portfolio that becomes harder to dig out of,” said Wade Pfau, professor of retirement income at the American College for Financial Services. “It is really the first 10 years of the market performance in retirement that are going to drive your outcome.”

While the S&P 500 lost 6.2 percent last year, the final three months of the year were especially volatile. It’s unclear where the market will go tomorrow, or the next decade. But whether you’re getting close to retirement or just starting to work, part of your financial success is a matter of chance: The growth of your portfolio is largely determined by when you started investing and when you retire.

Let’s say a person saved 15 percent of her earnings — a flat salary that grew with inflation — during a 30-year career. If that person retired in 1982, she would have accumulated just over five times her final salary. If she retired in 2000, however, she would have amassed 17 times her salary.

The same type of variability can occur based on the sequence of your market returns in retirement — except it’s amplified because instead of adding to the money you’ve invested, you’re spending it.

There are very simple strategies to try to reduce the effects of an ill-timed downturn or cancel them out altogether: Work longer or pick up a part-time job. Those aren’t feasible for people with health problems, or those who were laid off by their employers a few years shy of when they intended to retire. But they tend to be the most effective ways to help your money last.

Here are some other steps retirees can take to lengthen the life of their savings when markets are less than cooperative:

Portfolio Check. Retirees need to ask themselves a couple of key questions. Is my portfolio broadly diversified in low-cost investments, such as index funds? Is my allocation to stocks more than my stomach can handle should the market plummet 50 percent, as it did in 2008 and 2009?

If you answer “no” to these questions, you should reassess (preferably with a pro) how reducing your stock exposure might change your ability to spend what you want in retirement.

Mindful Spending. One of the most widely cited rules for retirement spending might be what’s known as the 4 percent rule. It suggests that retirees who withdrew 4 percent of their initial retirement portfolio balance, and then adjusted that dollar amount for inflation each year thereafter, would have created a paycheck that lasted for 30 years. (The numbers crunched by a financial planner more than two decades ago were based on a portfolio evenly split between stock and bonds.)

But if your portfolio value takes a significant hit, your withdrawal rate may have to increase to support your spending. If that rate starts to approach 5 percent, and certainly 6 percent, there’s a greater chance you’ll outlive your portfolio, Mr. Pfau warned. So adjustments may be in order.

The simplest way to deal with a dip would be to hold your spending steady, rather than increasing it with inflation. That approach can be enough to steady your finances even if your portfolio were to drop by 25 percent from its original value at retirement, according to Judith Ward, a senior financial planner with T. Rowe Price, based on a recent study. She suggested to keep spending steady for two to four years, depending on when the portfolio rebounds.

“Keep in mind, steady spending over a number of years may still result in some kind of spending cuts depending on the inflation environment,” she said. “That may be the easiest and most intuitive approach for many retirees.”

Create a Smoother Ride. Traditionally, investors reduce their exposure to stocks as they approach retirement. But one novel approach is to cut that exposure even further — then get back into the market as you age.

This strategy, studied by Mr. Pfau and Michael Kitces, director of wealth management at Pinnacle Advisory, is to increase your stock holdings over time. Portfolios that started with about 20 to 40 percent in stocks at retirement, and then gradually increased to about 50 or 60 percent, lasted longer than those with static mixes or those that shed stocks, according to their analysis.

Another option is to buy a guaranteed paycheck with a portion of your savings. With an immediate annuity, you pay a lump sum to an insurer in exchange for a guaranteed stream of income for life. A common approach is to consider how much of your must-have basic expenses — like food, shelter, property taxes — are covered by Social Security and any additional income, such as a pension. Then, buy enough annuity income to cover the gap. It also simplifies your financial life, which becomes increasingly important as you age.

But be careful with annuities: There are many types, and they can be complex — and not necessarily sold to you by someone who is legally required to put your financial interests ahead of his or her own.

Hold a Cash Reserve. If you’re approaching retirement and worried about a significant market correction, there’s another strategy that might provide some peace of mind: Keep up to two years of basic living expenses in cash to cover, say, the costs of housing, food and other essentials. With that sort of buffer, you can try to avoid tapping your investment portfolio for a while, giving it some time to recover.

Putting too much money in cash, however, may weaken overall returns because you will have less invested to begin with, and therefore less to build on.

Look for Higher Returns. This does not involve chasing after some hot stock or growing sector. It’s far more boring and counterintuitive, but guaranteed to deliver a higher paycheck in retirement over the long run: delay Social Security as long as you reasonably can.

“The effective return of delaying Social Security is much higher than what you will earn in the market today,” said David Blanchett, head of retirement research for Morningstar. “It is like a 10 percent guaranteed return.”

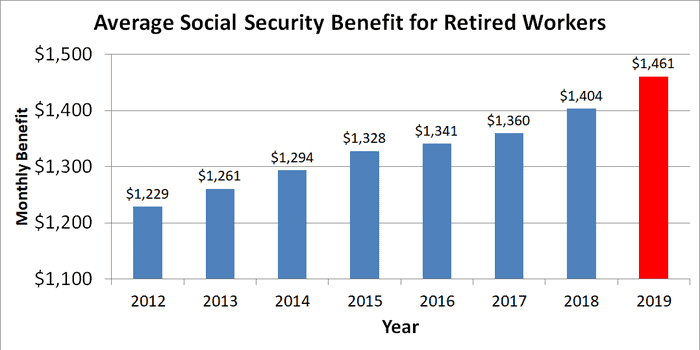

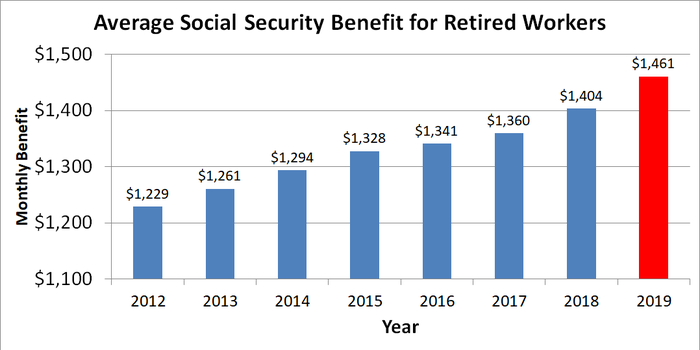

Your benefits generally rise by 8 percent for each year you wait to collect the check beyond your “full retirement age” — that is, the age you’re eligible for a full benefit, which is currently 66 years and 2 months for people born in 1955.

Someone set to receive a full benefit of $1,413 monthly (the average benefit amount), who instead waited two more years, would receive roughly $1,640 — an amount that would rise with inflation.

You can think of the money you don’t receive while you delay benefits as a payment for higher guaranteed income later on. And that payment buys you far more in annuity income than if you tried to buy it from a commercial insurer.

Get Help. If you doubt you have the strength to avoid temptation and stay the course — or you want assistance developing a coping strategy — this is the time to seek professional help. It can potentially make or break your retirement.

But you need to get the right type of help, which means avoiding salespeople and brokers who call themselves advisers but get paid only when they sell you something. Instead, find a certified financial planner who isn’t afraid to promise in writing that he or she will act as a fiduciary, which is legal speak for putting your interests ahead of their own.