If you’re retired, you’ve likely shifted from building your nest egg to trying to live off of your savings. That means you’ll want to look at stocks that are relatively safe and pay a generous dividend. Investors have punished the stocks of giant U.S. utility Southern Company (NYSE:SO) and packaged-food specialist General Mills (NYSE:GIS) for what are likely to be near-term problems, leading to big dividend yields.

Although each has some issues to deal with, the real risks are less than they appear for investors willing to think long term. Both should interest retired investors today.

1. A giant, high-yield utility

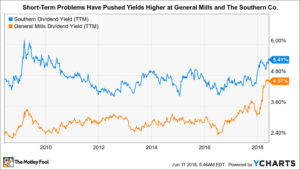

Southern is one of the largest electric and natural gas utilities in the United States. The stock is down 20% from the highs it reached in mid-2016. The yield is a robust 5.1%, more than twice the yield offered by an S&P 500 Index fund. And Southern’s beta, a measure of relative volatility, has been extremely low over the past five years, with the stock at times moving in the opposite direction of the overall market.

There are a few headwinds facing Southern today. First, rising interest rates have helped push the shares lower this year, but that’s an industrywide issue that Southern can’t do anything about. Second, Southern has a major nuclear power project, known as Vogtle, that hasn’t been going very well. It was over budget and missing key construction deadlines when its contractor Westinghouse declared bankruptcy last year.

But Southern has taken greater control of the project and switched to a new contractor. Since this change, the project has been hitting its key milestones.

The third issue is funding the company’s over $30 billion in capital spending plans, which notably include the nuclear power plants. This spending is expected to drive 4% to 6% earnings and dividend growth, but only if Southern can pay for it. On this front, the utility ended the first quarter with $6.2 billion in liquidity. It since has agreed to sell assets or interests in assets to raise additional cash, including a Florida utility and a piece of its solar business.

These moves should reduce debt and leave ample cash for capital projects once they’re consummated. Fears over massive dilutive stock sales, which have been hampering the shares lately, are unlikely to come to fruition.

Essentially, Southern has been addressing the issues it can control — funding investment plans and righting the Vogtle nuclear project. With the utility’s yield at the high-end of its range over the past decade, it would make a good addition to a retirement portfolio as it begins to deal with some of the concerns that have led to its relatively low share price.

2. A big deal, but risk is priced in

Next up is General Mills, the iconic packaged-foods company that owns name brands like Cheerios and Betty Crocker. Don’t look at the company as a food maker, however, because it’s really a brand manager. In fact, at a recent conference, CEO Jeffrey Hardmening made sure to point out that the company uses its global distribution system, product development skills, and advertising heft to support a collection of leading brands… that change over time.

The stock is down 40% from its 2016 highs and lower by nearly 30% in 2018 alone. That’s pushed the yield up to a very generous 4.4%. That’s at the high end of the historical range for General Mills’ dividend yield, making it worth a deep look from retired investors.

General Mills is facing three main issues. First, changing consumer tastes have led to weak sales for packaged-food makers. However, the company has been taking steps to adjust, and fiscal third-quarter sales were up 1% year over year. Not a great showing, but a solid one.

The second issue is profitability, which has been hampered by increasing costs, notably for transportation (profit margin fell 1.2 percentage points year over year in the quarter, to 15.7%). General Mills is planning on pushing through price increases to address this issue.

The third problem dragging General Mills shares lower today was the recent roughly $8 billion acquisition of fast-growing premium pet-food maker Blue Buffalo. This deal will push General Mills’ debt higher at a time when profitability is being constrained by rising costs. However, the company has stated that it’s committed to maintaining the dividend at the current level, with plans to focus on debt repayment over the next few years. That’s likely to include non-core asset sales.

With regard to integrating this new business, General Mills has a successful track record of taking on new brands, like Annie’s, and using its scale to broaden the acquired brand’s product lineup and distribution. The cost was material here, but the potential to leverage General Mills’ business strengths is huge.

The worst-case scenario is that the deal is a dud. But giant General Mills, despite notable leverage (long-term debt was around 60% of the capital structure before the Blue Buffalo deal), likely has the financial strength to muddle through such an outcome and keep rewarding investors with a hefty dividend. With such a large stock price decline, however, even this risk appears to be priced in today. Retired investors willing to take a long-term view of the situation should be taking a close look at General Mills.

Short-term thinking is your friend

Benjamin Graham is famous for saying that the stock market is a voting machine over the short term and a weighing machine over the long term. That’s a nice way to say that investors often get caught up in short-term issues that aren’t likely to have a major long-term impact on a company, pushing the shares lower temporarily. Southern and General Mills both appear to be dealing with short-term thinking today, creating a high-yield opportunity for investors willing to think long term.

This article originally appeared on Motley Fool.