Stock Markets

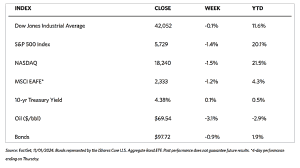

All the major indexes are down for this week. The 30-stock Dow Jones Industrial Average (DJIA) slipped down by 0.15% while the Total Stock Market fell by 1.16%. The broad S&P 500 Index dropped by 1.37% with losses among small-cap, mid-cap, and super-composite counters. The Nasdaq Stock Market Composite edged down by 1.50%, and the NYSE Composite gave up 1.04%. The CBOE Volatility Indicator (VIX), which tracks investor risk perception, rose by 7.62%.

On Wednesday, the technology-oriented Nasdaq Composite and the S&P MidCap 400 Index reached record intraday highs before sharply falling back on Thursday. Due partly to cautious earnings reports from Facebook parent Meta Platforms and software giant Microsoft, growth stocks generally lagged value shares. Small caps also outperformed large caps. Roughly 42% of the companies in the S&P 500 Index were expected to report third-quarter earnings over the week. Analysts expected that overall earnings for the S&P 500 would have increased by 5.1% compared to the same quarter one year ago. This would indicate a faster pace of growth than expectations before the start of the reporting season when analysts anticipated earnings to grow by 4.3%.

U.S. Economy

This week, data on two critical key factors were released ahead of the U.S. elections – corporate earnings growth and the U.S. labor market. According to the data, the economy is moderating but remains solidly positive. Earnings growth for the third quarter remains on track for 5%, which is slightly above expectations of approximately 4% growth at the start of the quarter. Earnings growth for the full year is expected to be 9%, well above last year’s 1% growth rate. The jobs report for October came in well below expectations. Some events, however, that may have distorted this reading were last month’s hurricanes and ongoing labor strikes. The labor market may be moderating, but it is not collapsing.

On Tuesday, the Labor Department reported that the number of job openings in September had fallen to its lowest level since January 2021 at.44 million. The number of Americans leaving jobs was relatively unchanged, as well as the number of those quitting voluntarily which is considered a better measure of labor market conditions. On Friday, however, the Labor Department reported that nonfarm payrolls were overall “essentially unchanged” over the month, with employers adding only 12,000 jobs. This is the lowest jobs numbers since December 2020. The impact reflected a decline of 44,000 jobs in transport equipment manufacturing activity due to the Boeing strike. There was little or no growth in employment in other major industries which should have compensated for the weakness.

Also, on Friday, the Institute for Supply Management’s gauge of manufacturing activity had unexpectedly dropped to 46.5. This is the seventh straight monthly decline and the lowest level in 15 months. According to the Institute, “Demand remained subdued as companies continue to show an unwillingness to invest in capital and inventory due to concerns about federal monetary policy direction in light of the fiscal policies proposed by both major parties.”

The softening of the macroeconomic data nevertheless signifies that the Federal Reserve is still on track to lower interest rates in both November and December this year. The economy that remains resilient combined with lower rates has historically favored financial markets broadly.

Metals and Mining

There is no doubt that precious metals saw significant momentum over the past month due to the volatile environment leading to the election. In the weeks leading up to November, the risk uncertainty continued to rise regarding anticipation about which political party would gain control over the White House and the two chambers of Congress. However, while the gold market is overdue for a correction, the fear of missing out, or FOMO, is growing in the marketplace as analysts note that dips are being aggressively bought up and surprising any remaining bears in the market. Gold has managed to hold support at every major breakout level in this step-by-step rally since July. In August it held support at $2,400, in September at $2,500, and in October at $2,600. As the U.S. economy and labor market slow, Gold continues to be well supported.

The spot prices of precious metals lost ground over the week. Gold, previously at $2,747.56, closed this week at $2,736.53 per troy ounce for a drop of 0.40%. Silver closed at $33.72 one week ago, and ended this week at $32.49 per troy ounce for a loss of 3.65%. Platinum, which closed at $1,025.29 one week ago, closed this week at $996.08 per troy ounce, for a loss of 2.85%. Palladium, with a closing price last week of 1,196.50, settled at $1,104.60 per troy ounce this week, losing 7.68% from last week. The three-month LME prices of industrial metals also generally fell with few exceptions. Copper began at $9,602.50 last week and fell by 0.33% to end at $9,570.50 per metric ton. Aluminum lost 2.89% from its close last week at $2,677.50 to end this week at $2,600.00 per metric ton. Zinc dropped by 1.05% from its ending price last week at $3,102.00 to close this week at $3,069.50 per metric ton. Tin, on the other hand, rose by 1.27% from its close last week at $31,325.00 to finish the week at $31,724.00 per metric ton.

Energy and Oil

Iran reemerged as the main talking point of the markets no sooner had OPEC+ depressed market sentiment by admitting a potential rollover of its cuts in 2025. Due to concerns about soft oil demand at the heels of China’s slowdown and rising non-OPEC supply, OPEC+ could postpone its planned increase in oil production. This move could bring back the 2.2 million barrels per day (b/d) output under eight countries’ voluntary cuts. Regarding geopolitical developments, the oil markets are now anticipating an Iranian attack on Israel, after the Israeli retaliatory strike had been downplayed. Iran is expected to respond with numerous drones from Iraqi territory. As a result, ICE Brent futures were lifted back to $74-$75 per barrel by a semblance of geopolitical risk premium, ahead of a highly uncertain week when the U.S. president is elected.

Natural Gas

For the report week from Wednesday, October 23, to Wednesday, October 30, 2024, the Henry Hub spot price rose by $0.03 from $1.91 per million British thermal units (MMBtu) at the start of the week to $1.94/MMBtu at the week’s end. Regarding Henry Hub futures, the November NYMEX contract expired on Tuesday at $2.346/MMBtu, up modestly from the previous Wednesday. The December 2024 NYMEX contract price decreased to $2.845/MMBtu, down by $0.06 over the report week. The price of the 12-month strip averaging December 2024 through November 2025 futures contracts declined by $0.03 to $3.038/MMBtu. Regional natural gas spot price changes were mixed this report week. Price changes ranged from a decrease of $0.12 at Eastern Gas South to an increase of $1.63 at PG&E Citygate.

International natural gas futures prices rose this report week. Weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia increased by $0.25 to a weekly average of $13.70/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, increased by $0.70 to a weekly average of $13.45/MMBtu. In the week last year that corresponds to this report week (beginning October 25 and ending November 1, 2023), the prices were $17.82/MMBtu in East Asia and $15.36/MMBtu at the TTF.

World Markets

European stocks lost ground in trading this week. The pan-European STOXX Europe 600 closed 1.52% lower in local currency terms, due to concerns regarding the potential for escalating conflict in the Middle East, poor corporate results for some companies, and moderating expectations for the European Central Bank (ECB) to further cut interest rates. The major stock indexes in the region also suffered from sell-offs. Italy’s FTSE MIB plummeted by 1.42%, France’s CAC 40 Index sank by 1.18%, and Germany’s DAX lost by 1.07%. The UK’s FTSE 100 Index slid by 0.29%. In the third quarter, the eurozone economy expanded by 0.4% sequentially. Encouragingly, this exceeds the consensus estimate of 0.2% and is double the second-quarter growth rate. France and Spain reported stronger-than-expected economic growth. So did Germany which unexpectedly avoided a recession and grew by 0.2%. However, Italy’s economy stalled. Meanwhile, as the decline in energy prices last year dropped out of the annual comparison, the annual headline inflation accelerated slightly faster than forecast to 2% in October from 1.7% in September. The core rate (excluding energy, food, alcohol, and tobacco prices) remained unchanged at 2.7%. Services inflation also remained constant at 3.9%.

Japan’s stock market climbed over the week. The Nikkei 225 Index gained by 0.4% and the broader TOPIX index advanced by 1.0% as the Bank of Japan (BoJ) kept interest rates steady amid political uncertainty. In the country’s lower house election on Sunday, October 27, Japan’s ruling Liberal Democratic Party (LDP)-Komeito coalition failed to secure a majority, as the opposition capitalized on public discontent with the higher cost of living and the LDP corruption scandal. In an effort to maintain control of the lower house, Prime Minister Shigeru Isheba faces the prospect of a minority government as it sought the support of smaller parties. Initially, the yen weakened against the U.S. dollar on the outcome of the election on expectations that a period of political uncertainty would follow and potentially impact the BoJ’s monetary policy and future fiscal policy. The BoJ held its policy rate steady at 0.25% at its October meeting, aligning with expectations. By the end of the week, the yen traded within the JPY 152 range against the greenback, virtually unchanged. In the central bank’s view, the economic risks in the U.S. had broadly diminished which the market has taken to suggest that conditions could be aligning for another rate hike. Market participants are divided on whether this would come as early as December of this year or January of next year.

Chinese equities pulled back this week despite data showing that economic activity had begun to pick up. The Shanghai Composite Index lost 0.84%, while the blue-chip CSI 300 declined by 1.68%. The Hong Kong benchmark Hang Seng Index gave up 0.41%. The country’s factory activity grew for the first time since April due to growing demand. According to the statistics office, the official manufacturing purchasing managers’ index (PMI) rose from 49.8 in September to an above-consensus 50.1 In October, moving from contraction to expansion. The nonmanufacturing PMI, which is the gauge for construction and services activity, rose to a lower-than-expected 50.2 in October from 50 in September. Increased spending during the country’s Golden Week holiday partly accounts for the rise in services activity. On the other hand, the private Caixin/S&P Global survey of manufacturing activity advanced from 49.3 in September to 50.3 in October amid new order growth. Regarding the property sector, the value of new home sales by the country’s top 100 developers rose by 7.1% in October year-on-year compared to September’s decline of 37.3%. According to the China Real Estate Information Corporation, this marks the first year-on-year growth in 2024. Overall, the first batch of major economic indicators after the rollout of Beijing’s stimulus package point to early signs of recovery in the Chinese economy.

The Week Ahead

In the coming week, look forward to important events including the U.S. presidential election, the FOMC meeting, and the release of the preliminary report on U.S. productivity for the third quarter.

Key Topics to Watch

- Factory orders for Sept.

- S. trade deficit for Sept.

- ISM services for Oct.

- S&P final U.S. services PMI for Oct.

- Initial jobless claims for Nov. 2

- U.S. productivity (prelim) for Q3

- Wholesale inventories for Sept.

- FOMC interest-rate decision

- Fed Chair Powell press conference (Nov. 7)

- Consumer credit for Sept.

- Consumer sentiment (prelim) for Nov.

Markets Index Wrap-Up