In today’s era of Venmo and Zelle, where you can transfer money to your friends with the press of a few buttons, personal checks can feel very antiquated.

And they are!

But some people, and companies, still require you to write them a check.

Just the other day, we had to write a check to pay a mere $4 for our son’s recorder. Sometimes that’s just the way it is.

So if you’ve been asked to send a personal check, but aren’t exactly sure how to do it, we have you covered.

Here are the steps to filling out a personal check.

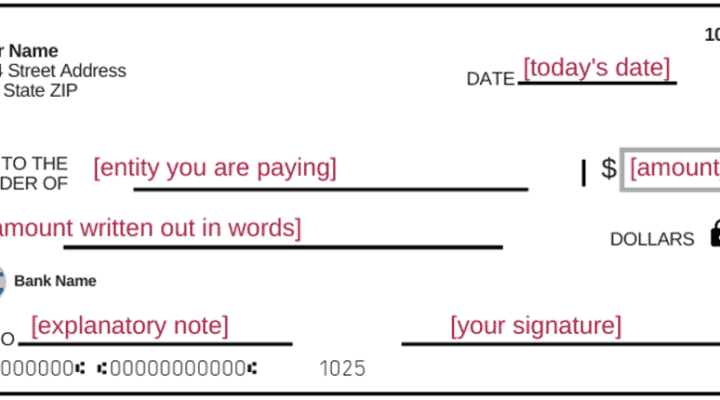

6 Easy Steps to Filling Out A Personal Check

As you can see in the above example, the steps are pretty easy and straightforward:

- Write in the date for the check, typically today. You can put a day in the future, thus “post dating” the check.

- Write in the name of the payee (you are paying this person) on the “Pay to the Order Of” line

- Write in the amount of the check, in numbers, in the box to the right.

- Below the “Pay to the Order Of” line, write in the amount of the check in full words. So, $2,345.67 would be written as “Two thousand, three hundred forty five and 67/100”

- Write a short note in the Memo line if necessary. Some companies ask you to put your account number or your name in this field.

- Sign it.

A personal check has a lot of security features and it’s important you fill it out properly or the bank could reject the check.

For example, the amount in the box has to match the amount written out on the check itself. It’s to prevent someone from adding numbers to the box after the fact.

How to Void A Check

Sometimes you’ll need to give someone a “voided” check. If this is the case, you can just write VOID in big letter across the check. This makes sure the bank won’t accept it as a valid check.

In many cases, they want a voided check so they get your bank details so don’t cover up the routing number and account numbers at the bottom of the check.

For example, if your company’s HR department wants a voided check to set up direct deposit, they’ll ask for a voided check.

Try to Avoid Using Checks

I try to avoid using personal checks because of how much sensitive information is on the check itself. The check has your address, your bank’s information, plus your account number on it.

If you can avoid it, use other payment methods but sometimes that’s all a company accepts.