Everyone knows profit growth is poised to cool this year. But by how much? Analysts who try to answer that question by looking at signals embedded in the stock market are coming up with some worrisome numbers.

Going by history, the 16 percent decline in the S&P 500 between Sept. 20 and Jan. 3 reflected investors pricing in better-than-even odds of an economic recession in 2019 and a 9 percent decline in earnings, JPMorgan strategists led by Nikolaos Panigirtzoglou wrote in a note. Another approach, the dividend discount model, suggested markets anticipate annual profit growth of 3.7 percent through 2023, according to Goldman strategists led by David Kostin.

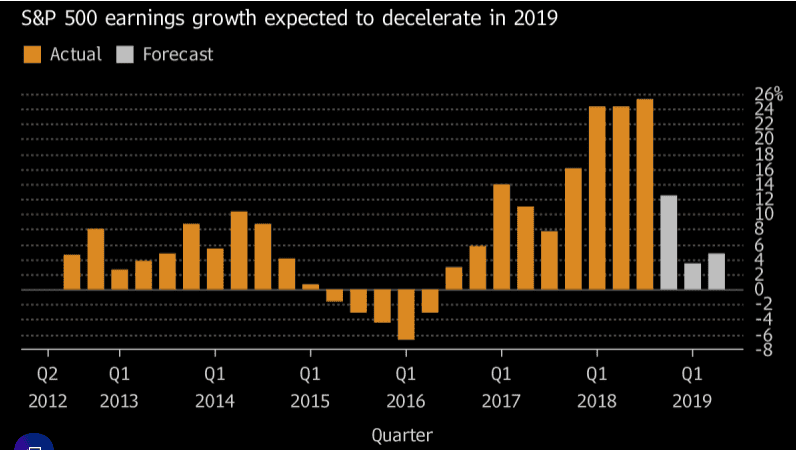

Either is a far cry from the consensus estimate of individual stock analysts, who as of Friday predict earnings in the benchmark will rise 7.7 percent this year. And both are a major downshift from the 20 percent-plus increase companies will post for all of 2018.

The divergence is raising the urgency of the upcoming reporting season, which begins next week. Have investors sussed out weakness that has yet to show up in professional estimates? Or maybe volatility got ahead of itself in the worst December for stocks since the Great Depression.

“The market is looking for direction,” Kathy Fisher, head of wealth and investment strategies at AllianceBernstein, said in an interview on Bloomberg TV. “The earnings we’ll see the next few weeks will be very important to give some sense of direction.”

U.S. stocks are bouncing back after the S&P 500 last month fell to the brink of a bear market decline of 20 percent. Up for six out of the last eight days, the index has extended the post-Christmas rally to almost 9 percent. The JPMorgan and Goldman models examined the period through last week and tried to fashion a forecast of what the market was saying.

“Equities are already pricing a very sharp slowdown in growth and profits,” strategists led by Goldman’s Peter Oppenheimer wrote in a note Monday. “What matters now, therefore, is not so much a deterioration in data but rather how far it deteriorates relative to current negative expectations.”

The decline in S&P 500 prices over the past 12 months pointed to a reading below 50 in the Institute for Supply Management’s manufacturing index, or a contraction, Goldman’s models suggested. While the gauge last month plunged to a two-year low, at 54, it still indicated an expansion.

Earnings anxiety is mounting as investors started to question the sustainability of a cornerstone of the 10-year bull market. From the absence of a boost from tax cuts to currency headwinds, weaker global demand to rising wages, the list of threats to corporate profits is getting long.

And with sales warnings rising among firms like Apple Inc. and Delta Air Lines Inc., analyst estimates may have nowhere to go but down. Over the past three months, expected profits for 2019 have fallen 2.7 percent to $172 a share, data compiled by Bloomberg showed.

To Mike Wilson, chief U.S. equity strategist at Morgan Stanley who predicts a 50 percent chance for two consecutive quarters of negative profit growth to occur in 2019, the market has reflected that call. Once analysts are done with downgrades, stocks will be able to stage a sustained rally, he said.

“Investors are bearish and their positioning reflects that bearishness,” Wilson wrote in a note. “That’s a good thing, and exactly what we have been waiting for to get more constructive.”