Shares of The Home Depot (NYSE:HD) and Sherwin-Williams (NYSE:SHW) have both crushed the market over the past decade, helping investors earn fortunes along the way.

But which of these home-improvement giants is the better buy today? Read on to find out.

THESE STOCKS CAN HELP YOU ADD SOME MORE GREEN TO YOUR PORTFOLIO. BUT WHICH IS THE BEST BUY NOW? IMAGE SOURCE: GETTY IMAGES.

Competitive advantage

Sherwin-Williams is the market leader in the $125 billion paint and coatings industry. Unlike many of its competitors, the company’s vast network of retail stores allows it to cut out the middleman and interact directly with its customers. This gives it an informational advantage, helping it to innovate and adapt to changing consumer trends faster than its rivals. Moreover, its strong brand gives it pricing power, or the ability to consistently raise prices without severely impacting sales. Together, that’s helped Sherwin-Williams deliver nearly five times the gains of the S&P 500 over the past decade.

SHERWIN-WILLIAMS STOCK PERFORMANCE, DATA BY YCHARTS.

Like Sherwin-Williams, Home Depot is a dominant force within its industry. Its more than $100 billion in annual revenue dwarfs that of No. 2 home-improvement retailer Lowe’s, which checks in at less than $70 billion. This size and scale help Home Depot earn industry-leading returns on capital and generate strong free cash flow, which it passes on to shareholders in the form of a rising dividend and sizable share repurchases.

HOME DEPOT STOCK HIGHLIGHTS, DATA BY YCHARTS.

All told, both Sherwin-Williams and Home Depot are strong, competitively advantaged businesses. Of the two, though, I believe Home Depot — as a retailer — is more exposed to the threat posed by e-commerce juggernaut Amazon.com. Sherwin-Williams, which also manufactures its products, is more insulated from this risk. Home Depot has done an admirable job of defending its market share up to this point, and the company has solid plans in place to further fortify its defenses against online competitors. However, I’m going to give the edge to Sherwin-Williams for its more defensible economic moat.

Advantage: Sherwin-Williams

Financial fortitude

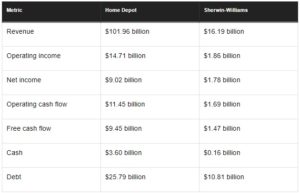

Let’s now see how Home Depot and Sherwin-Williams compare on some important financial metrics.

It’s easy to see that Home Depot is the far larger and more financially powerful business, with nearly $3.5 billion more in cash reserves, five times the net profit, and six times the free cash flow of Sherwin-Williams.

Advantage: Home Depot

Growth

Thanks largely to its acquisition of Valspar, Sherwin-Williams is projected to increase its revenue by 18% in 2018 and nearly 6% in 2019. Home Depot, meanwhile, is expected to grow its sales by about 7% this year and 4% next year.

As for earnings per share, Wall Street is forecasting that Sherwin-Williams’ EPS will rise at a 15% annualized clip over the next five-years, as the company realizes more of the benefits of its Valspar acquisition. Home Depot is also projected to increase its earnings about 15% annually during this period, fueled by its “One Home Depot” strategy and additional share repurchases.

Still, due to its greater expected revenue growth, I’ll give the edge to Sherwin-Williams here.

Advantage: Sherwin-Williams

Valuation

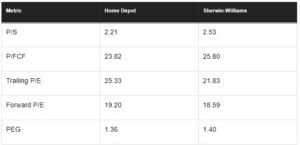

Finally, let’s take a look at some valuation metrics for these two retailers.

Home Depot’s shares are less expensive on a price-to-sales and price-to-free cash flow basis, while Sherwin-Williams shares are cheaper on both a trailing and forward price-to-earnings basis. And these two stocks’ PEG ratios are essentially the same, which makes sense since they’re expected to grow their EPS at basically the same rate over the next half-decade. So, I’m going to call it a draw in terms of valuation.

Advantage: Neither

The better buy is…

With these two home-improvement stocks trading at similar valuation levels, Sherwin-Williams’ more defensible competitive position and greater revenue growth prospects make it the better buy today.

This article originally appeared on The Motley Fool.