Alexei Kulikov was charged with looting a small Moscow bank. But his trial turned into a window on the shadowy—and seemingly uncontrollable—world of money laundering in Putin’s Russia.

The pounding on the door begins at about 6 a.m. on a wintry Moscow day in March 2016. Insistent knocking at that hour usually means just one thing: police.

Inside the apartment on tony Kutuzovsky Prospekt, Alexei Kulikov’s partner, Maria Plyushkina, 23, cares for their infant son. She begs Kulikov not to open the door. The 40-year-old banker, stunned by the possibility of arrest, knows better than to consider that option. Ignoring the appeals from the men outside but desperately seeking help, he starts making calls—first to his lawyer, then to any and every friend who might have some pull with law enforcement. It’s all for nothing. He’s alone.

The officers take Kulikov, who’d celebrated his birthday just days earlier, to the headquarters of the Investigative Department of the Russian Ministry of the Interior near the Kremlin on suspicion of defrauding a bank in which he owns a stake. Questioned until 4 the next morning, he denies any wrongdoing. Later that day, a judge at Tverskoi District Court in Moscow orders him held without bail.

Kulikov hasn’t been home since. Charged with fraud and embezzlement and facing a 10-year prison sentence, he went on trial in March in the Podolsk City Court, just south of Moscow. The main allegations centered around the alleged looting of 3.3 billion rubles from Promsberbank, a small lender that the Central Bank of Russia had shut down about a year before Kulikov’s arrest.

By Russian standards, it was pretty typical treatment for a businessman in trouble with the law. Kulikov’s arrest got little notice in the local media. He lived large, driving a Mercedes-Benz SLR sports car and hiring stars from Comedy Club, Russia’s hottest TV-comedy show, to perform at a birthday party, says an associate, who spoke on condition of anonymity because of the sensitivity of the case. But he was no oligarch. As for Promsberbank, it looked like just another casualty in regulators’ efforts to clean up the financial sector. Its collapse drew scant attention beyond its home base in the gritty suburb of Podolsk.

Despite appearances, Promsberbank was, according to the central bank, a “crucial link” in one of the biggest money laundering schemes ever exposed in Russia. Kulikov wasn’t charged with laundering funds, but from its unprepossessing office on Kirov Street, his bank helped pump more than $10 billion out of Russia, the regulator says. Promsberbank was a key conduit into a channel that used stock transactions called “mirror trades.” These transactions involved buying shares of Russian blue-chip stocks through local brokers in Moscow for rubles and simultaneously selling them in London for dollars or euros, effectively bypassing regulations to move funds out of the country. Some of the laundering benefited members of President Vladimir Putin’s inner circle, say people familiar with the investigations. Igor Putin, the son of the younger brother of the president’s father, served on Promsberbank’s board of directors before regulators shuttered it.

To help avoid detection, the brokers in Moscow made these trades through big Western banks, according to Russian regulators. The bulk of them went through Deutsche Bank AG from 2012 to 2014. Revelations about the mirror trades, first reported by Bloomberg News in 2015, rocked Germany’s largest lender, already battered by legal troubles and fines in the wake of the financial crisis. Deutsche Bank admitted to “systemic” failuresin its internal controls, shut down its Russia trading desk, and agreed to pay a total of $630 million in fines to the U.K.’s Financial Conduct Authority and the New York State Department of Financial Services for lax anti-money laundering practices. The U.S. Department of Justice is pursuing a criminal investigation in the case.

Russia’s treatment of Deutsche Bank wasn’t quite so harsh. Regulators fined it 300,000 rubles, praised it for cooperating, and closed the case. Although Kulikov’s criminal prosecution makes no mention of the German lender by name, investigators did quiz several witnesses in detail about Deutsche Bank and the mirror trades, say lawyers and witnesses in the case.

At his trial, Kulikov pleaded his innocence and said he was being made the fall guy for the more powerful players who really controlled Promsberbank. Only Kulikov was charged in the Promsberbank affair, but the names of his partners in the bank read like a who’s who of Russian money laundering. Two of the bank’s investors, Igor Putin and Alexander Grigoriev, were shareholders in Russky Zemelny Bank, which was shut down for suspicious activities in 2014 after being linked to a $20 billion-plus money laundering scheme, an operation so large it came to be known simply as the “Russian Laundromat.”

Another apartment, another time. In September 2016 police turn up at No. 284 on the 11th floor of the newly completed Dominion luxury complex near Moscow State University. They’re there as part of an investigation into corruption allegations against a police colonel named Dmitry Zakharchenko. They remove the door with power tools. Nobody is home, but something gets their attention: a custom-built vault. Inside, police find so much cash—$124 million and €1.5 million ($1.7 million)—that it takes them all night to count it. It’s stashed in wine boxes and plastic tote bags embossed in faux-Burberry plaid. There are bricks of stiff $100 bills shrink-wrapped in $100,000 bundles.

The raid on Kulikov’s home may not have made headlines in Moscow, but the story of the Dominion vault did. Investigators still haven’t publicly disclosed where the huge amount of cash came from. Local media reports were full of speculation about the money’s origins: the strongrooms of failed banks or maybe bribes and other illicit payments known as chorny nal (black cash). Zakharchenko was charged with abuse of office, bribery, and obstruction of justice. He said in a court hearing in August that the charges were “fabricated.” Further hearings in his case, which hasn’t gone to trial yet, were declared closed to the public because prosecutors feared the disclosure of sensitive information. Zakharchenko said he didn’t live in the apartment, which belonged to his sister. She didn’t actually live there either. Apparently, only the money did.

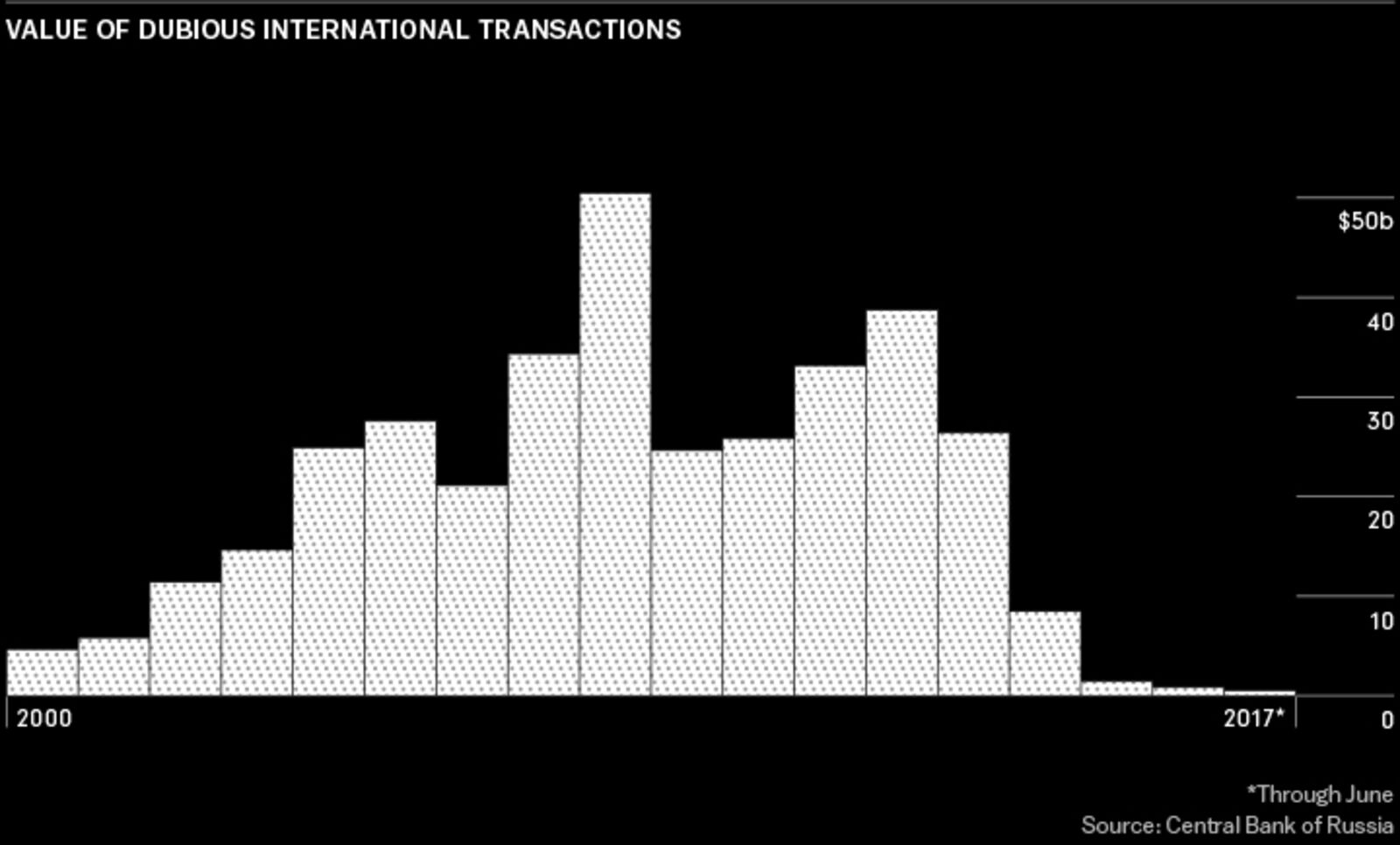

As with the Dominion stash, some illicit funds, whether proceeds of crime or business profits that the wealthy want to conceal from the Kremlin’s prying eyes, stay home, perhaps to be used for crooked or off-the-books dealings. But huge tranches of it—as much as $100 billion a year, according to official estimates—flow out of Russia into safe havens. VTB Group, one of the country’s biggest state banks, says wealthy Russians keep three-quarters of their money outside the country.

To stay ahead of regulators, money launderers frequently alter the complex chains of transactions, banks, and front companies they use to get the money out of Russia and into the global financial system. Mirror trades were a favored conduit in the first half of this decade, regulators say, but they’ve been replaced by other mechanisms for moving money, including illicit reinsurance contracts and fraudulent court orders. Other laundering channels seek to take advantage of weak regulatory environments in former Soviet nations such as Moldova.

“It’s always easier to steal money than it is to earn it,” says Pavel Medvedev, ombudsman at the Association of Russian Banks. But then you need to clean it and keep it safe, which explains why so much of it ends up outside Russia. “The protections for money overseas are better,” Medvedev says. He would know: As a member of parliament representing Kremlin-aligned parties for two decades, he helped write much of Russia’s banking law. “In Russia,” he says, “the rules of the game aren’t reliable, the shadow economy is very big, and corruption is high.”

For years, Russian regulators fought a losing battle to stem the outflows. But after tensions with the West surged in the 2014 Ukraine crisis, and U.S. and European Union sanctions targeted the overseas wealth of President Putin’s inner circle, the Kremlin began to put more muscle behind the crackdown. Putin called on Russia’s rich to bring their money home to strengthen the country’s economic defenses. The plunge in the price of oil, Russia’s main export, only intensified the need to bring back the cash. “Economic security became more important than the loyalty of the elite,” says Kirill Kabanov, a member of a Kremlin advisory panel and head of an anticorruption group. “It became political.”

Publicly, senior Russian officials insist the crackdown on illicit financial flows is working. But in private, they admit the effort has targeted mainly low- and midlevel players, leaving the masterminds behind the huge trade largely untouched. That’s certainly the way Alexander Lebedev sees it. Lebedev, a frequent Kremlin critic, is a banker and former member of parliament who’s investigated money laundering. “Individual bankers are arrested,” he says, “but, as a rule, it’s usually for small-time things.”

During his trial, Kulikov sat behind the corrugated bars of a defendant’s cage, a signature element of any Russian criminal courtroom. Thin and bookish, wearing rimless glasses, taking notes on the proceedings in a thick notebook, the banker projected an academic air. Indeed, as he recalls during a break one day, he used his time in jail to complete a doctoral dissertation on Russian economics, adding to the law degree he already has.

Kulikov, a native Muscovite, was a relatively low-profile player in the city’s financial world for years before he invested in the bank that would land him in jail. He dabbled in politics. In 2007 he was one of more than 500 parliamentary candidates put up by a pro-Kremlin socialist party that won only 39 of 450 seats. Kulikov, who lost, wasn’t exactly a fixture on the campaign trail. “The only time I saw him was in his picture on the campaign poster,” says Alexei Andreyev, who was on the party ticket in the same region.

When he ran for office, Kulikov listed his job as “adviser to the chairman” of Kreditimpex Bank, a midsize lender in Moscow. He also appears to have been a shareholder: A company he owned, OOO Ordkom, is listed in public disclosures as having a 20 percent stake in the bank. Investigators raided Kreditimpex’s Moscow offices in March 2013, alleging the bank had been part of a scheme to launder 8 billion rubles in fraudulent tax refunds on imported goods, according to Russia’s Investigative Committee. While there’s no indication that the criminal case progressed any further, the central bank revoked Kreditimpex’s license a year later, citing unspecified regulatory violations.

By that time, Kulikov already had a backup in place. Promsberbank was founded in 1990 during the twilight of Soviet communism. The bank’s name is an abbreviated version of Russian for “Industrial Savings Bank,” and in those days the lender focused mostly on financing factories in Podolsk along the Pakhra River. Never very ambitious, Promsberbank was ranked 264th by assets among Russian banks at the end of 2012.

Around that time, the bank’s original owners sold out to Kulikov and his associates, including Igor Putin, who became one of seven board members, and Grigoriev. Kulikov took a 19 percent stake. Together with his co-investors, he paid 1.8 billion rubles for control of the bank. The new owners took over Promsberbank with plans to turn it into a major player, according to court documents. They moved quickly, former employees would later tell investigators. New clients got massive loans days after opening accounts, a radical departure from the previous management’s go-slow approach. One of the bank’s executives later testified that file folders pertaining to big new clients were marked with the letter “A” to denote VIP handling. As transaction volumes surged, longtime clients found themselves sidelined, according to court records.

Kulikov, meanwhile, was aiming high. Twice during the year after buying into Promsberbank, he visited the Moscow headquarters of Deutsche Bank’s Russian operations, seeking to persuade the German lender’s top executive there to open a correspondent account for Promsberbank, according to Kulikov’s statement to police on the night he was arrested. Such an account would have allowed Promsberbank to do business through Deutsche Bank. (Deutsche Bank declined to comment.) There’s no indication Kulikov succeeded.

No matter. Kulikov and his associates still managed to do billions of rubles in business with Deutsche Bank.

The mirror trades began in 2012, according to Deutsche Bank’s internal investigation. Among the first participants was a Moscow brokerage company, IK Financial Bridge. It was one of several local players that placed big orders with Deutsche Bank in Russia to buy large blocks of popular Russian blue chips such as Lukoil and Sberbank. Simultaneously, seemingly unconnected companies based in the U.K. or one of its overseas protectorates, the British Virgin Islands, placed matching sell orders for the same shares in the same amounts with Deutsche Bank in London. The German lender paid them the proceeds in dollars or euros.

The mirror-image transactions—thousands of them over a four-year period—didn’t yield any profit on the stocks, because they were conducted usually within moments of each other. This wasn’t about making money; it was about moving money.

Russian regulators eventually caught up with Financial Bridge, revoking its license in August 2013 for repeatedly violating securities and money laundering laws. By then, however, according to the central bank, the mirror trades had been diverted to other brokerages. One was Lotus Capital. According to Russian central bank records, Lotus paid for its side of the mirror trades with rubles from an account at Promsberbank. It held the stocks it bought through Laros Finance, a share depository that was also owned by Kulikov’s Promsberbank associates.

By late 2014 regulators were closing in on the network. They’d been tipped off by the large volumes of trades that all seemed to go one way, either all buying or all selling. In April 2015, Deutsche Bank cut off Lotus Capital after the central bank warned that Lotus was conducting suspicious transactions. In October, again after being alerted by the regulator, Deutsche Bank stopped doing business with another mirror-trade brokerage, Rye, Man & Gor Securities. And once again, Kulikov entered the picture.

A longtime fixture in Moscow, Rye Man had recently come under new ownership and become an active mirror-trader. When its chief executive arrived at Deutsche Bank’s Moscow offices to lobby for a reprieve on the ban, he brought along Kulikov. Kulikov held no position at Rye Man. He told a convoluted story to explain his presence, according to a statement given to police by a Deutsche Bank official who was there. Kulikov said the investors behind the trades Deutsche Bank had found suspicious were in fact clients of a Cypriot bank. (He later told police he was a part-owner of a Nicosia-based bank, which he said was planning to buy Rye Man.) But he refused to name the investors or explain where the money for the transactions came from.

Deutsche Bank’s compliance staff was unimpressed and demanded an explanation for the sudden surge in one-way trades and for where the money was coming from. They never got one.

Kulikov didn’t give up. After the meeting, according to his police statement, he called a Deutsche Bank compliance officer and demanded an urgent meeting. They met in the Kofemania cafe on the ground floor of Deutsche Bank’s Moscow building.

According to Deutsche Bank’s internal report, Kulikov told the compliance official it was vital that the German bank resume trading with Rye Man, insisting the transactions were legitimate. Then, according to the account the compliance official later gave the police, Kulikov said he had an “unofficial proposal” for the compliance officer and discreetly slid his cellphone across the table. The screen showed “0.1-0.2% of monthly volume,” the official told police. He said he refused what he understood to be a bribe, which he later reported to Deutsche Bank. Asked about this during a break in his trial, Kulikov confirmed the meetings but denied offering a bribe.

By this time, Deutsche Bank’s mirror-trading days were numbered. Within two months, in February 2015, Russian police turned up at the bank’s Moscow office to investigate a fraud case against Lotus Capital, the broker with the accounts at Promsberbank. Then, within days, top Deutsche Bank executives ordered the internal probe that would expose the billions in mirror trades. By the spring, several Moscow staffers at the bank had been suspended, and all the clients involved were cut off.

Even so, the mystery would get murkier. Regulators would discover that the mirror-trading customers were connected to each other through common directors, owners, employees, or addresses. But all those connections, according to a U.K. Financial Conduct Authority report earlier this year, were merely “intermediaries that traded on behalf of undisclosed underlying clients.”

In the meantime, Promsberbank was running into trouble of its own. The aggressive expansion under its new owners, including sloppy lending to dubious clients, had left the bank overextended and short of cash. Auditors from the central bank pored over the bank’s records at the end of 2014 and found numerous instances of loans with little or no collateral, Promsberbank’s longtime chief accountant would later testify.

The regulator demanded that the bank set aside heftier reserves for the loans, but there was no money to offset potential losses. By March 2015 the bank didn’t have enough cash to cover the withdrawals by nervous depositors amid a run on the bank. Files on some of the biggest loans deemed dubious by the regulators disappeared when they were moved from one office to another, according to court documents. On April 2 the central bank revoked Promsberbank’s license. Less than three months later, the Moscow Region Arbitration Court declared it bankrupt.

Alexander Sharkevich, an elite Interior Ministry undercover cop investigating money laundering, stops his Lexus near Moscow’s Bolshoi Theatre, opens the window, and exchanges words with a man standing on the corner. As Sharkevich puts the car back in gear, the man tosses a package through the still-open window. Agents of the Federal Security Service (better known by its Russian acronym, FSB) swarm in, surprising Sharkevich, who steps on the gas and takes off. The FSB agents catch up to him a few miles away, where he’s been trapped in Moscow’s legendary traffic.

The package contains €350,000 in cash. After a two-hour standoff, Sharkevich tries to explain that he’s working undercover, assigned to worm his way into the confidence of a high-level money launderer. The FSB agents arrest him anyway. After a year and a half in jail, he manages to beat the corruption charges in 2009. But the suspected money launderer he was targeting has gone free—shielded, Sharkevich says, by high-level protection within the security services.

Now retired, Sharkevich offers a unique view of money laundering. He says it’s wired as deeply into Russia’s police and security apparatus as it is into business and finance. Bankers engaged in laundering often enjoy unofficial dispensation for their illicit businesses, which arms of the state themselves can use for everything including monitoring criminal flows and funding covert operations abroad. If the moneymen get caught and come to a “bad end,” he says, it’s usually because their powerful protectors have lost their jobs. “These bankers provide various services supposedly in the interests of the state,” Sharkevich says. In return, he says, “the bankers are allowed to not only break the law but also to take money out of the country.”

Whether Kulikov was scapegoated in the Promsberbank case to protect people more powerful than he may never be known. He testified in court that he was just small fry, a minority shareholder with a 19 percent stake, and a dutiful son who gave the shares to his mother as a 70th birthday present. He didn’t sit on the board of directors. He didn’t even have a title.

The 437-page indictment against him portrays him rather differently. He was the ringleader who put together the investor group to buy the bank in 2012, installed allies in key management posts, and began pumping out huge loans to new clients. Most of them were companies with no real operations—“one-day firms,” as they’re known in Russian business parlance—that never paid back the loans, prosecutors said.

Kulikov’s partners in the Promsberbank takeover had a long record in the Russian financial industry—mostly involving failed banks. Igor Putin joined the Promsberbank board when Kulikov and the other investors took over, according to court documents. He left the board in 2014. By that time, two other lenders in which Putin was involved had been shut down by regulators. In a statement to the Russian press that year, he said he was getting out of banking and called for the industry “to be cleansed of banks headed by people with dubious reputations.” He has since disappeared from the public eye and couldn’t be reached for comment for this story.

One of the failed banks Igor Putin was involved in—along with Promsberbank investor Grigoriev—was Russky Zemelny Bank, the largest single player in the notorious Laundromat affair. The Russian central bank puts the total amount of money run through the Laundromat over a period of about 18 months at $21 billion, most of it funneled through the impoverished former Soviet republic of Moldova; government investigators have said the figure could be twice that much. Russia’s Novaya Gazeta newspaper, along with the Organized Crime and Corruption Reporting Project, linked 70,000 transactions, 1,920 companies in the U.K., and 373 in the U.S. to the scheme. Grigoriev has been in jail since November 2015, charged with setting up a criminal organization at two other banks he owned. Through his lawyer, he denies those allegations and says he sold his Promsberbank stake before the crimes with which Kulikov is charged took place. Despite Igor Putin’s and Grigoriev’s somewhat lofty perches in the pantheon of Russian banking, Kulikov didn’t finger them as masterminds behind the Promsberbank affair. He pointed to another one of his investment partners: Ivan Myazin.

Myazin’s office in downtown Moscow isn’t the kind that draws attention to itself. There’s no name on the door. The place is barely furnished. Myazin, 53, is flanked by his lawyer as he gives his first-ever interview. He’s slender and dressed in an expensive-looking blue blazer and jeans. He makes no apologies for his association with Vyacheslav Ivankov, a legendary Russian organized-crime boss known as “Yaponchik” (Little Japanese), who was gunned down on a Moscow street in 2009. “He was a quiet, smart, simple man,” Myazin says. “We used to celebrate New Year’s together with our families.”

But Myazin says that association doesn’t make him a crook. He’s a “financial consultant” with no shortage of clients, he says, though he declines to identify any of them. Yes, three banks he’s invested in, including Promsberbank, all had their licenses revoked, he says, but that’s the result of overzealous regulators, not any wrongdoing on his part. As for the banker Lebedev’s allegation that he was “one of the creators” of the Laundromat operation, Myazin denies it, adding, “I got squeamish when I heard about it.”

Myazin says Kulikov approached him in 2012 about investing in Promsberbank. “When Kulikov pitched the bank [to me], it looked like a sweetheart—only 0.3 percent bad loans,” he says. Adding to Myazin’s confidence in the Promsberbank deal was that Grigoriev, the now-jailed financier of Russky Zemelny Bank fame, was on board as a co-investor. “I’ve known Sasha Grigoriev since before he was a banker,” Myazin says. “He was a well-known fixer. He had great contacts.” Financial Bridge, the early mirror-trader, also participated, advising on the deal and holding stakes for some shareholders, Myazin testified.

In the runup to Kulikov’s trial, the police questioned Myazin. He was never charged in connection with the Promsberbank affair. But he was definitely in the courtroom to testify against his erstwhile partner.

It’s a June day in Podolsk, midway through Kulikov’s trial. The defendant is in his cage, glowering. Myazin is at the witness stand, talking up Kulikov’s stature at Promsberbank. “Of course, Alexei played a very active role in the activities of the bank,” Myazin testifies. “He had a very weighty vote.”

Kulikov objects, saying it was Myazin, after all, who’d signed the employment contract hiring Boris Fomin, the Promsberbank chairman who allegedly went into hiding after his name showed up on a wanted list in connection with defrauding the bank. Judge Diana Almayeva orders Kulikov to be quiet.

Later in the proceedings, Kulikov’s lawyer, Tatyana Galimardanova, presses Myazin on the contract issue—his signature is right there. “That’s surprising to me,” he admits. “There’s no way I should have signed that protocol, but I see my signature.”

Shortly before the end of the trial, Kulikov gets a chance to question Myazin directly. The back and forth grows tense. When Kulikov presses Myazin on whether he was aware of the theft of assets from the bank, the judge shuts him down. “Don’t get carried away, Kulikov,” she says without further explanation, moving quickly to wrap up the testimony.

Four months later, in October, Judge Almayeva begins reading her verdict aloud, as Russian court procedure requires. It takes almost a full week to get through the 400-odd pages. Her voice grows hoarse and hurried as she recites the arguments, accepting those of the prosecution and dismissing those of the defense. The final verdict and sentence come on a rainy Friday morning: guilty, nine years in prison.

On one of the visitors’ benches, Kulikov’s mother sobs. Plyushkina, Kulikov’s partner, tries to comfort her, saying there’s still a chance for appeal. (His lawyers would file one a few weeks later.) In the defendant’s cage, Kulikov turns pale, lowers his face into his hands, and leans against the bars, tears welling up in his eyes. His hands grip the metal shafts so tightly his knuckles turn white.

“Is the verdict understood?” Judge Almayeva asks.

“Yes, your honor,” Kulikov says.

Reznik and Pismennaya are senior reporters for Bloomberg News in Moscow. White is an editor in Moscow. With assistance from Ksenia Galouchko and Alexander Sazonov.