REUTERS/Brendan McDermid

Billionaire investor Warren Buffett made a lot of people feel better about historically stretched stock prices earlier this month.

Speaking in an interview with CNBC on October 3, the chairman and CEO of Berkshire Hathaway said, “Valuations make sense with interest rates where they are.”

The investment community breathed a sigh of relief. After all, Buffett is arguably the most successful stock investor in world history. An all-clear from him surely gives a green light for adding more equity exposure, right?

Wrong, says John Hussman, the president of the Hussman Investment Trust and a former economics professor.

In his mind, Buffett only gets half of the equation right. While Hussman acknowledges that low lending rates do, by nature, improve future cash flows, he argues that they must also be accompanied by strong growth — something that he notes the US is not currently enjoying.

To Hussman, the simple idea that “lower interest rates justify higher valuations” is one that gives people false confidence.

“It’s an incomplete sentence,” Hussman wrote in a recent blog post. “Unfortunately, the convenience of investing-by-slogan, rather than carefully thinking about finance and examining evidence, is currently leading investors into what is likely to be one of the worst disasters in the history of the U.S. stock market.”

Hussman calculates that stock valuations are stretched 175% above their historic norms, and predicts the S&P 500 will see negative total returns over the next 10 to 12 years. Along the way, the benchmark index will experience an interim loss of more than 60%, he estimates.

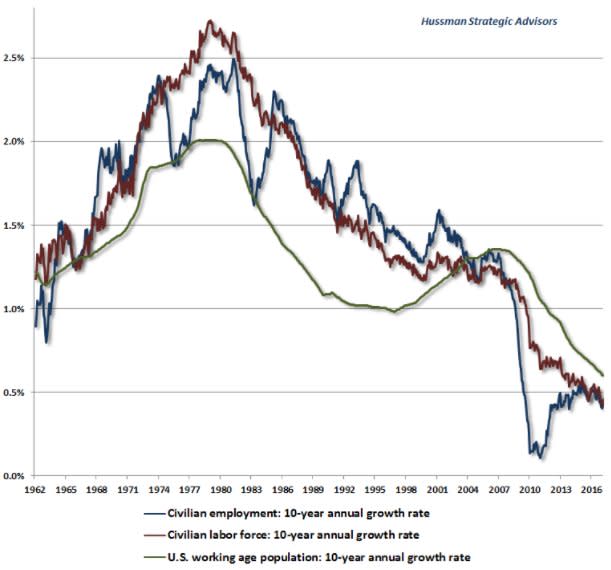

As touched on above, at the core of Hussman’s bearish argument is a lack of economic growth. He specifically points to slowing expansion in the US labor force, as shown by this chart:

Hussman Strategic Advisors

“Put simply, if interest rates are low because growth rates are also low, no valuation premium is ‘justified,'” Hussman wrote. “The long-term rate of return on the security will be low anywaywithout any valuation premium at all. This observation has enormous implications for current U.S. stock market prospects.”

So where does that leave the market at this very moment? In the very near term, Hussman’s neutral, citing the continued speculative impulses of investors. Still, he stresses that traders should be hedging and using other safety nets to protect against potential downside, which he says could materialize quickly.

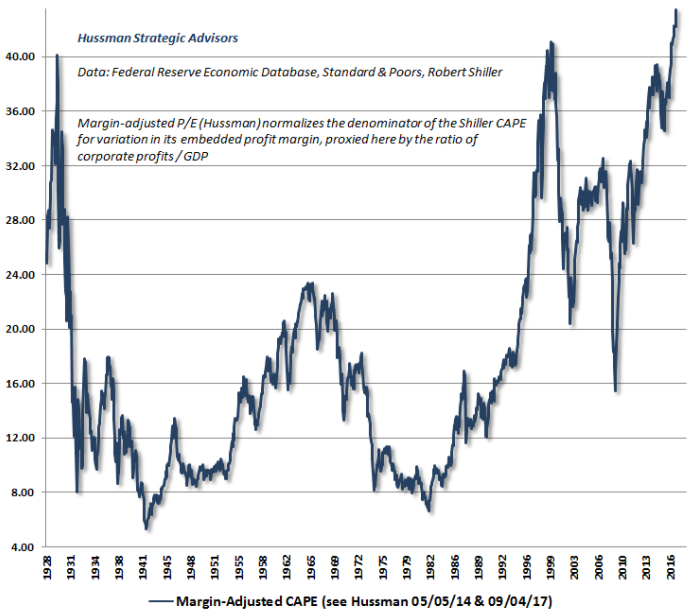

To say he’s less than warm and fuzzy about the stock market is an understatement. And when discussing price levels, he doesn’t exactly pull any punches, saying US equities are now “at the most offensive level of overvaluation in history” — even worse than in 1929 and 2000.

We leave you with the chart supporting Hussman’s bearish claims, which shows the margin-adjusted price-earnings ratio for the US stock market at a record high:

Hussman Strategic Advisors