Stock Markets

Stocks were mixed last week as investors weighed lawmakers’ approval of a long-awaited relief bill against ongoing virus concerns and new U.K. travel bans. Small cap and technology stocks were up, with both the Russell 2000 and Nasdaq indexes finishing the week higher. The U.S. has continued its vaccination effort, with over 1 million people receiving the first dose of the new vaccine. The president has cast doubt over the passage of the new relief bill, but analysts think it is likely to pass because it contains key funding for vaccine distribution. Consumer confidence has seen a short-term dip, and weekly jobless claims rose unexpectedly, pointing to continued strain from economic restrictions across the country.

US Economy

The year 2020 will go down in history as one of the most memorable and unpredictable years of our lives. The pandemic and resulting health crisis upended everyone, creating unique challenges for individuals, businesses and governments. From a financial-markets perspective, 2020 was a year of unprecedented change but eventual resiliency. As governments imposed strict lockdowns to buy time for the health care systems that were threatened to be overwhelmed, the economy plunged into a deep self-induced recession. However, swift and aggressive policy support helped prevent this health crisis from evolving into a prolonged, full-blown financial crisis. With a week left to go in the year, the light at end of the tunnel is brighter as a result of the medical breakthroughs around vaccine development. Major market indexes are trading near record highs, reflecting a positive 2021 outlook, an outcome that was hard to envision during the early days of the pandemic.

Energy and Oil

Crude oil prices moved higher as the week ended after the Energy Information Administration reported an inventory draw of 600,000 barrels for the week to December 18. This compared with a draw of 3.1 million barrels estimated for the previous week and an inventory build of 2.7 million barrels for the week to December 18, as estimated by the American Petroleum Institute and reported Thursday. Analysts had expected the EIA to report an inventory draw of 3.25 million barrels for last week. Oil prices have been on the rise the past two weeks on positive vaccine news and hopes for a rebound in demand once vaccinations started on a large scale. However, earlier this week, oil reversed its climb on the news about a new, more virulent variant of the coronavirus infecting thousands in the UK and prompting new travel restrictions in Europe and other parts of the world. The news saw oil traders exit their positions in droves, driving prices down. A decline in crude oil buying by Asian refiners also contributed to the most recent reversal of oil prices’ fortunes. Meanwhile, the EIA reported an inventory decline in gasoline, to the tune of 1.1 million barrels, with production last week averaging 8.8 million bpd. This compared with an inventory build of 1 million for the week before last and average production of 8.5 million bpd. Natural gas spot prices rose at most locations this week. The Henry Hub spot price rose from $2.45 per million British thermal units (MMBtu) last week to $2.67/MMBtu this week. At the New York Mercantile Exchange (Nymex), the price of the January 2021 contract increased 24¢, from $2.442/MMBtu last week to $2.677/MMBtu this week. The price of the 12-month strip averaging January 2021 through December 2021 futures contracts climbed 20¢/MMBtu to $2.780/MMBtu.

World Markets

Shares in Europe were roughly flat for the week ended Thursday, as hopes for a UK-European Union (EU) trade deal helped reverse sharp losses caused by the emergence of a new variant of the coronavirus.

The UK and the EU finally agreed on a post-Brexit trade deal, with the announcement coming after UK markets closed. The accord still must be approved by all EU member states. The agreement’s terms would represent a significant change in the relationship with the UK’s major trading partner and, some say, amounts to a “hard” Brexit in all but name. The Office for Budget Responsibility has forecast that Brexit will cost the UK 4% of its gross domestic product (GDP) over 15 years.

The EU approved the Pfizer-BioNTech vaccine for COVID-19, the disease caused by the coronavirus. The companies said they would supply 12.5 million doses to the EU by the end of the year, Reuters reported. The EU Commission also doubled its orders for Moderna’s vaccine to 160 million doses, with delivery expected to start in early 2021.

China’s benchmark stock index fell for the week ended Thursday as a flareup in Sino-U.S. tensions weighed on sentiment. The Shanghai Stock Exchange (SSE) Composite Index shed 1.0% over the four days ended Thursday, while the large-cap CSI 300 Index was nearly flat. On Monday, the Trump administration published a list of Chinese and Russian companies that it alleged had ties to their countries’ militaries. The list of 58 Chinese and 45 Russian companies requires a license for anyone seeking to sell them items that could be used for military purposes, according to a Commerce Department statement. The SSE Index recorded its biggest one-day percentage drop since September after the list was published, which marked the latest instance of U.S. actions targeting Chinese companies as President Trump prepares to leave office.

In corporate news, Alibaba Group made headlines after China’s top antitrust regulator announced Thursday that it started an investigation into the e-commerce giant. Separately, Chinese regulators said that they have summoned Ant Group, the world’s largest financial technology company and Alibaba affiliate, to a high-level meeting regarding financial regulations. The coordinated actions show that Beijing is ramping up efforts to rein in the domestic tech companies that it sees as a threat to political and economic stability as the companies have grown larger and more powerful in just a few years.

The Week Ahead

Important economic data being released next week include pending home sales and the Chicago PMI.

Key Topics to Watch

- S&P Case-Shiller home price index

- Advance report on trade in goods

- Chicago PMI

- Pending home sales

- Initial jobless claims (state program, SA)

- Initial jobless claims (total, NSA)

- Continuing jobless claims (state program, SA)

- Continuing jobless claims (total, NSA)

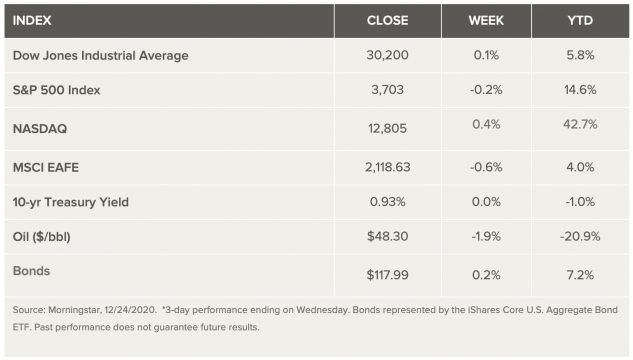

Market Summary