Not every stock that pays a dividend is a “great dividend stock.” The best dividend stocks are from many different industries, but share some common traits. Not only do they need to pay a relatively high dividend yield, but the payout should be sustainable and should also have room to grow steadily over time.

With that in mind, here are three of my favorite dividend stocks in the market, all of which I would feel comfortable buying and holding for years to come.

Company (Symbol) Industry Recent Share Price Dividend Yield

National Retail Properties (NYSE: NNN) Real estate – Retail $39.78 4.7%

U.S. Bancorp (NYSE: USB) Banking $51.33 2.3%

AT&T (NYSE: T) Telecommunications $32.28 6.2%

Data source: TD Ameritrade. Stock prices and dividend yields as of 5/14/18.

Think all retail is in bad shape? Think again

Many investors are hesitant to put any money into the retail industry, and with the wave of retail bankruptcies, store closures, and once-mighty retailers like Sears struggling to survive, who could blame them? However, National Retail Properties is a different story.

National Retail Properties is a real estate investment trust, or REIT, that exclusively focuses on net-leased retail properties. The vast majority of the company’s tenants are engaged in areas of retail that aren’t exposed to the same e-commerce headwinds that are hurting so many brick-and-mortar retailers today. Service-based and non-discretionary businesses make up most of National Retail’s portfolio — think businesses like convenience stores, restaurants, and fitness centers, just to name a few. The top three tenants are 7-Eleven, Mister Car Wash, and Camping World, and there are about 2,800 properties altogether in the company’s portfolio.

The proof is in the numbers. National Realty’s adjusted funds from operations per share (the REIT version of earnings) is up by 11.7% year over year, and it finished the first quarter of 2018 with impressive 99.2% portfolio occupancy.

National Retail Properties’ e-commerce and recession-resistant tenant base and the company’s solid balance sheet have allowed the company to increase its dividend every year for the past 28 years in a row — and there’s no reason to think this streak is in jeopardy.

A bank in a class by itself

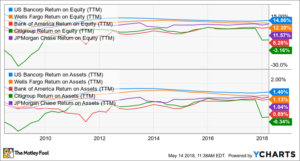

When it comes to the biggest banks in the United States, there are two main categories in terms of profitability and efficiency — U.S. Bancorp and everyone else. In terms of return on equity (ROE), return on assets (ROA), and efficiency ratio, U.S. Bank (the blue lines in the chart below) is consistently well above its peers.

In a nutshell, U.S. Bancorp’s management simply does an excellent job of managing risk and running its operation efficiently. This is why it didn’t get hit nearly as badly during the financial crisis as its peers, never recording a single net loss during that time period. In many ways, U.S. Bancorp emerged from the crisis even stronger.

In fact, the Federal Reserve’s 2017 banking stress tests found that not only would U.S. Bancorp survive a hypothetical “deep recession,” but the bank would actually remain profitable.

This telecom leader has several growth catalysts

From an income investor’s standpoint, it’s tough not to like AT&T. The stock pays a juicy 6.2% dividend yield, it has low volatility (beta of just 0.5%), and its dividend payout rate has been increased for more than 30 years in a row.

However, there are also reasons to like AT&T from a growth perspective. For starters, AT&T is aggressively investing in 5G technology, and if it brings this new, faster version of wireless data transmission to market sooner (or more effectively) than peers, it could be a big revenue driver. This is especially true with the surge in connected devices that’s expected over the next decade or two, such as driverless cars, “smart home” devices, and more.

In addition, its acquisition of DirecTV gives the company a big edge over rivals like Verizon when it comes to content delivery. In fact, many investors are surprised to learn that AT&T is now the largest pay TV provider in the U.S., and its DirecTV Now streaming service has been gaining serious traction and could be a major differentiator going forward. This content-delivery advantage could be further amplified if the company’s pending merger with Time Warner clears its regulatory hurdles.

In short, AT&T is more than just a big dividend. It is a high-income stock with long-tailed growth opportunities ahead.