Investing in companies that are capable of maintaining a high level of performance can be a life-changing event. The best of these stocks will be worth holding for decades, then passing down to your children as heirlooms that continue to build wealth for your family.

To help readers identify a selection of stocks that might fit this profile, we assembled a panel of three Motley Fool investors and asked each member to spotlight a company that’s on track to go the distance. Here’s why they think that Five Below (NASDAQ: FIVE), Square (NYSE: SQ), and Walt Disney (NYSE: DIS) are stocks that you and your family should own for the ultra-long term.

Image source: Getty Images.

A stock tweens won’t grow out of

Dan Caplinger (Five Below): Everyone likes a bargain when they’re shopping, but for teens and preteens, low prices are especially important because of the limited financial resources that many young shoppers have. Five Below puts an emphasis on stocking trendy items for the tween market at prices between $1 and $5, making it possible for the budget-conscious to get the items they want at an affordable price. With everything from workout gear to fidget spinners, Five Below stays in touch with what’s hot in retail and works with suppliers to keep the price right.

From an investing standpoint, Five Below has seen its stock double since late 2015. With a store count that continues to rise and a devoted customer base, the tween retailer has managed to boost sales per square foot even in a retail environment that’s been decidedly unfriendly to most of Five Below’s peers. The company also just came off its best holiday season since its initial public offering almost six years ago, with same-store sales climbing 6.7%. Five Below has itself dialed into what its customers want, and long after they’ve grown up and stopped shopping there, kids who were smart enough to spend some money investing in Five Below shares aren’t likely to let their parents forget it.

Enabling an explosion in small businesses

Travis Hoium (Square): Starting a small business is hard work, and navigating the payroll, accounting, inventory, and payments can be a headache for any founder. But Square makes the process easy through a software platform and card reader that are among the easiest to use on the market. It’s a go-to company for small businesses and has expanded capabilities to provide a complete solution to these customers.

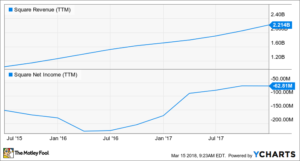

Square’s growth has primarily been driven by improving adoption by small businesses, like food trucks, breweries, and other small vendors. Where Square has sought growth in the last few years is in larger organizations with over $500,000 in annual payment volume. These customers accounted for just 13% of volume in Q4 2015 but had grown to 20% of payment volume in Q4 2017. Long-term, these customers will both help increase revenue and provide a more predictable volume of cash.

As you can see, Square hasn’t been able to turn a profit, but losses are getting smaller and the company is leveraging revenue growth to slowly expand margins. Management expects the improvement to continue, with guidance for 2018 GAAP loss per share improving slightly to $0.04 to $0.08. On an adjusted basis, earnings are expected to be $0.43 to $0.47 per share.

At its core, Square enables people to start new businesses and takes a cut of the growth they’re enabling as compensation. It’s the kind of business model that enables innovation and is a good deal for everyone involved. I think that’s the kind of stock your kids will brag about someday.

Let Mickey Mouse work for your house

Keith Noonan (Walt Disney): With a business model that thrives on synergy between its segments, a growing returned-income profile, and a cheap valuation, Disney is a stock that’s worth buying and holding for the ultra-long term. Shares trade at just 15 times forward earnings amid some market skepticism about the company’s outlook, and that presents investors with an opportunity to buy a great company at a great price.

The big source of the uncertainty surrounding Disney stems from threats facing its media networks segment. ESPN has been at the core of the company’s earnings engine over the last two decades, and declining ratings and cord-cutting point toward a future of declining profits from the unit. Disney isn’t standing still on the issue, however. The company will soon launch a direct-to-consumer ESPN-branded streaming service that should create a supplementary sales stream and provide some valuable data for shaping the network’s digital future. The media networks’ situation certainly isn’t ideal, but much of the doom and gloom appears premature and seems to overshadowing Disney’s long list of strengths.

The company has a collection of characters and franchise properties that’s head-and-shoulders above that of any other media company, and it also has a proven track record of creating new hits. That’s an advantage that will only become more pronounced with the acquisition of Twenty-First Century Fox’s film assets. It’s also one that extends far beyond the box office, with blockbuster properties also giving the company an edge in readying its own Netflix-like streaming platform, driving traffic to theme parks and resorts, spurring merchandising sales, and providing content for its television networks.

Disney deserves plaudits as a dividend growth stock as well. Shares yield about 1.6% at current prices, and the company has roughly doubled its payout over the last five years and still has plenty of room for growth. Taken together, I think Disney has what it takes to stand the test of time and deliver wins for your family for many years to come.